(Click here for Blog Archive)

(Click here for Blog Index)

(Presentations in this blog were created using the InsMark Illustration System.)

|

|

Editor’s Note: Blog #128 (Part 2) may be easier to follow if you take the time to review Blog #127 ( Part 1) assuming you haven’t already done so. |

Continuing our study of the Leveraged Executive Bonus Plan for Alex Demas as described in Blog #127, let’s next examine a feature that can be added to it that could guarantee Alex’s continuing employment for at least the next 10 years.

In Blog #127 we discussed that Hawthorne Construction, Inc., decided that part of a new benefit plan for Alex will include a Leveraged Executive Bonus Plan funded with $2,875,000 of indexed universal life (IUL). The policy is max-funded with five level premiums of $100,000 paid for with deductible bonuses by the company paid to Alex. Alex will offset the resulting income tax liability on each bonus by way of a bank loan secured against the IUL.

This is an impressive executive benefit! No out-of-pocket cost for Alex coupled with $4.8 million in after tax retirement cash flow, all provided by Hawthorne Construction for an after tax cost of $65,000 a year for five years.

Click here to review Alex’s Leveraged Executive Bonus Plan from the InsMark Premium Financing System. (Pages 8 and 9 show the Summary numbers.) We used the Income Tax Financing module in the InsMark Premium Financing System to prepare the illustration.

Controlled Executive Bonus

If a Controlled Executive Bonus feature is added to Alex’s benefit plan, it means he would be required to repay all (or, perhaps, only part of) the bonuses if he were to voluntarily terminate employment within a certain number of years. It could also be based on a certain event like reaching retirement or achieving a specific company goal.

With this feature, Hawthorne Construction can select a certain percentage payback of the bonus (e.g., 100% in all 10 years) or schedule a variable percentage payback, e.g., 100% during year 1, declining by 10% a year over the next 9 years.

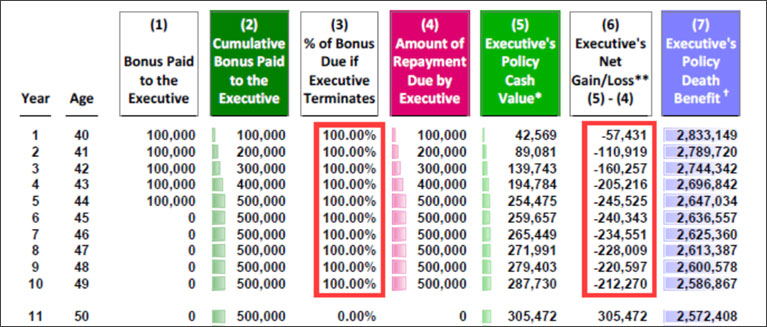

Below is an example of a Controlled Bonus repayment schedule for Alex using “voluntary termination prior to 11 years” as the duration in which a 100% repayment is required. Please understand that Column (3) is an example of only one of many possible repayment schedules.

Possible Repayment Schedule

**Negatives in Column (6) are in excess of policy cash values. The financial gain in Alex’s favor between the 10th and 11th year is in excess of $500,000 ($212,270 + $305,472), a powerful incentive to remain employed.

† The typical Controlled Bonus Plan agreement provides that the repayment obligation is waived at the executive’s death if it occurs during years of a repayment obligation.

The repayment obligation could be extended longer than 10 years -- perhaps until retirement. Instead of that, I suggest it would be much more productive for Hawthorne Construction to launch a similar plan for Alex when he is age 50 assuming the firm remains anxious to retain him.

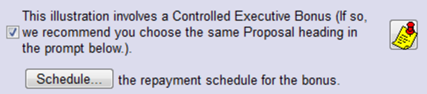

Click here for a review of the details of the bonus repayment feature from the InsMark Illustration System.

Note: The Controlled Executive Bonus repayment feature is not currently available in the Income Tax Financing module in the InsMark Premium Financing System. It is available in the Executive Bonus Plan and Executive Security Plan modules in the InsMark Illustration System -- and that is the source I used for the screen shot above and the link in the prior paragraph. We will be adding this feature to the Income Tax Financing module in the InsMark Premium Financing System in the near future.

Suppose Alex elects not to participate. In this case, the company will have discovered that he may be considering alternative employment and is not interested in a benefit plan with such a short-term contingent liability. Clearly, Alex’s decision not to participate would uncover valuable business information that might otherwise be difficult to determine, and this could allow the firm to plan accordingly.

Alternative Benefit Plans

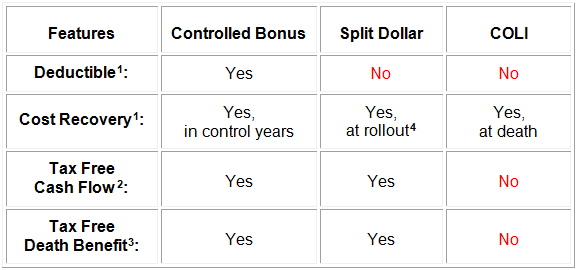

In many ways, a Controlled Bonus is superior to loan-based split dollar and salary continuation (COLI) plans:

1 to employer 2 to executive 3to executive’s family 4 typically at retirement

Since the loss of equity split dollar in 2003, Executive Bonus Plans have become one of the premier go-to executive fringe benefits. Using a bank to finance the executive’s income tax on bonus plans takes them to a new and better level. Adding the Controlled Bonus features adds a new dimension to retention of important non-owner executives and minority shareholders.

Sarbanes-Oxley eliminates the use of Loan-Based Split Dollar for executives of public corporations; however, this does not apply to loans made by an executive where no corporate liability exists for the loan. The Leveraged Executive Bonus Plan featured in this three-pronged Blog series should be usable by any private or public business entity.

Licensing InsMark Systems

To license the InsMark Illustration System, visit us online or contact Julie Nayeri at julien@insmark.com or 888-InsMark (467-6275). Institutional inquiries should be directed to David Grant, Senior Vice President ? Sales, at dag@insmark.com or (925) 543-0513.

InsMark’s Digital Workbook Files

If you would like some help creating customized versions of the presentations in this Blog for your clients, watch the video below on how to download and use InsMark’s Digital Workbook Files.

Digital Workbook Files For This Blog

Download all workbook files for all blogs

|

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark System. Please forward the Workbook where you can launch it on your PC where your InsMark System(s) are installed. |

Testimonials

“Standard bank financing illustrations produce much in the way of great data, but it takes the InsMark Premium Financing System to really present compelling numbers; however, the integration of that data into InsMark’s comparative modules like Various Financial Alternatives and Wealthy and Wise is really what makes premium financing sizzle.”

Chris Jacob, CFP, SFI-Cadeau, St. Louis, MO, InsMark Platinum Power Producer?

“As with all of the InsMark software, InsMark’s Premium Financing System has proven to be an indispensable addition to my ability to show my clients the advantages in using bank loans to solve their financial needs. Because of this, I was able to close three large financed cases easier and faster than ever before. As always, InsMark has delivered again. I encourage all who use bank financing as a solution to their clients’ needs to purchase this system. The cost of the system is not an expense, but rather an investment in your business.”

William Moates, Jr., Trilennium Financial Alliance LLC, Fort Smith, AR, InsMark Platinum Power Producer?

“InsMark has created without question the best suite of software for our industry that has ever existed. I personally have been using their software for almost 30 years, and it changed my career. This unique and user friendly software will add many thousands to your income for as long as you’re in business. InsMark makes me look good, and it will you as well.”

Simon Singer, CFP?, CAP?, RFC?, International Forum Member, InsMark Platinum Power Producer?, Encino, CA

Important Note #1: The hypothetical life insurance illustrations associated with this Blog assumes the nonguaranteed values shown continue in all years. This is not likely, and actual results may be more or less favorable. Actual illustrations are not valid unless accompanied by a basic illustration from the issuing life insurance company.

Important Note #2: Many of you are rightly concerned about the potential tax bomb in life insurance that can accidentally be triggered by a careless policyowner. Click here to read Blog #51: Avoiding the Tax Bomb in Life Insurance.

Important Note #3: The information in this Blog is for educational purposes only. In all cases, the approval of a client’s legal and tax advisers must be secured regarding the implementation or modification of any planning technique as well as the applicability and consequences of new cases, rulings, or legislation upon existing or impending plans.