(Click here for Blog Archive)

(Click here for Blog Index)

(Presentations in this blog were created using the InsMark® Illustration System)

|

Supplemental Executive Retirement Plans (SERPs) have long been the go-to benefit plan for large public companies, and the new 21% income tax bracket for C corporations frees up substantial cash flow for such plans. SERPs typically include retirement and survivor benefits (both taxable to the covered executive or his beneficiaries) and are funded with corporate-owned life insurance (COLI) policies.

A variation I like features after tax retirement and survivor benefits. It is called Endorsement Split Dollar with Salary Continuation at Retirement (ESD+SC), and this is how it works:

A business purchases cash value life insurance on a valuable executive and sets it up as endorsement split dollar. It extends the right to the insured executive to name beneficiaries of a portion of the policy death benefit. The executive’s taxable economic benefit is the value of the life insurance coverage which is calculated using specific term insurance-type tables, typically IRS Table 2001. This produces phantom income to the executive on which income tax is due. The sponsoring company generally pays a bonus to cover the tax on this income resulting in no out-of-pocket cost for the executive. Policy loans by the employer fund the after tax cost of the salary continuation benefit at retirement.

A primary advantage of ESD+SC vs. COLI is the death proceeds of ESD+SC paid to a covered executive’s personal beneficiaries are free of income tax. A COLI plan generally provides all survivor benefits as taxable compensation.

Case Study

Jennifer Dexter Bailey, age 45, is a new senior officer of Western Gas and Electric Company (a C corporation). In her position, she is entitled to an ESD+SC plan.

Here are the details of Jennifer’s plan:

- Policy: Indexed universal life (IUL) owned by Western Gas and Electric.

- Face amount: $ 2,200,000 (increasing death benefit option for 30 years; level after that).

- Annual premium: $56,000 for 20 years (paid by Western Gas and Electric).

- Cash value of the policy: Owned by Western Gas and Electric in all years.

- Jennifer’s pre-retirement, personal share of the policy death benefit: $2,000,000.

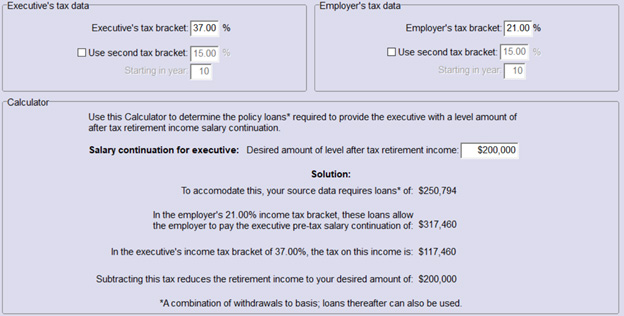

- Starting at Jennifer’s age 65, Western Gas and Electric elects ten, annual, participating, tax free, policy loans of $250,794 which it grosses up to pay $317,460 to Jennifer from age 65 to 75. In her 37% income tax bracket, she nets $200,000 after tax each year.

Important Note (if you want to illustrate this concept): There is a critical series of calculations available on the first tab of the Endorsement Split Dollar with Salary Continuation at Retirement module located on the Split Dollar tab of the InsMark Illustration System. You should use this feature to establish the necessary data for your life insurance illustration:

- At retirement, Jennifer’s $2,000,000 share of the policy death benefit continues for another ten years.

- Jennifer must recognize phantom income in years 1 - 30 calculated by multiplying a term-type rate table issued by the government (Table 2001 rates) times each $1,000 of the death benefit payable to her personal beneficiaries. Western Gas and Electric pays her a relatively small bonus to offset the income tax cost of this economic benefit.

- After 30 years, all benefits for Jennifer cease and, as illustrated, Western Gas and Electric continues the policy in force for recovery of its costs.

Below is a graphic of the overall results of Jennifer’s plan:

| Image 1 |

| Endorsement Split Dollar |

| with Salary Continuation at Retirement |

Click here to review the entire illustration.

Conclusion

The results for Jennifer are impressive: $2,000,000 of tax free, life insurance death benefit for 30 years and $2,000,000 of tax free, retirement cash flow – all for no out-of-pocket cost to her.

Thanks to the arbitrage available in IUL, should Western Gas and Electric desire, the plan has sufficient residual cash value at the end of 30 years to continue $100,000 of annual, after tax cash flow for Jennifer starting at age 75 and continuing for 25 years to her age 100.

Note: Some may wonder why I calculated the after tax amount of salary continuation at retirement as SERPs generally illustrate before tax benefits. I did so for two reasons:

- I believe it is a more realistic number for a client to evaluate (as you can see in the Conclusion above).

- Many of our licensees reflect the impact of executive benefits within InsMark’s Wealthy and Wise®, and that System deals solely with after tax results.

Note: Some may question whether loan regime split dollar or executive bonus might be better choices for Jennifer. Endorsement Split Dollar with Salary Continuation at Retirement is designed for an employer who wants to reflect all policy cash values on its balance sheet and also welcomes the presence of key person indemnification through its share of the policy death benefit.

Note: S corporations have a different cost structure for Endorsement Split Dollar with Salary Continuation due to the absence of the 21% income tax bracket. I have included an example for an S corporation in the digital workbook file for Blog #182 available below. Due to the new pass-through rules affecting S corporations, there are a variety of tax bracket possibilities. The one I included in the workbook assumes no benefit from the new pass-through rules.

Specimen Documents

InsMark’s Cloud-Based Documents On A Disk™ (“DOD”) has specimen documents for Endorsement Split Dollar with Salary Continuation at Retirement in the Employer-Sponsored Split Dollar Plans section of documents in Business Owner Benefit Plans. If you are licensed for DOD, go to www.insmark.com and select “My InsMark” from the home page for access to the full version of DOD.

InsMark’s Cloud-Based Documents On A Disk™ (“DOD”) has specimen documents for Endorsement Split Dollar with Salary Continuation at Retirement in the Employer-Sponsored Split Dollar Plans section of documents in Business Owner Benefit Plans. If you are licensed for DOD, go to www.insmark.com and select “My InsMark” from the home page for access to the full version of DOD.

If you are not licensed for DOD, this link will take you to the DOD product site for more information or you can contact Julie Nayeri at Julien@insmark.com or 888-InsMark (467-6275). Institutional inquiries should be directed to David Grant, Senior Vice President — Sales, at dag@insmark.com or (925) 543-0513.

Licensing InsMark Systems

To license the InsMark Illustration System, visit us online or contact Julie Nayeri at Julien@insmark.com or 888-InsMark (467-6275). Institutional inquiries should be directed to David Grant, Senior Vice President — Sales, at dag@insmark.com or (925) 543-0513.

Creating Similar Presentations

If you would like some help creating customized versions of the presentations in this Blog for your clients, watch the video below on how to download and use InsMark’s Digital Workbook Files.

Files For This Blog

New Zip File Downloaders

Watch the video.

Experienced Zip File Downloaders Download the zip file, open it, and double click the Workbook file name to open it in your InsMark System.

|

Before downloading and reviewing any files, be certain you have installed the most current updates to your InsMark Systems. Do this using Live Update available under Help on the main menu bar of the System or this icon on the main menu bar:

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark Systems. Please forward the Workbook where you can launch it on your PC where your InsMark System(s) are installed. |

If you obtain the digital workbook for Blog #182, click here for a guide to its content. It will be invaluable to you.

Note: In the event that Jennifer is employed by an S corporation instead of a C corporation, Blog #182 contains a second proposal using that assumption.

Testimonials

“InsMark has created without question the best suite of software for our industry that has ever existed. I personally have been using their software for almost 30 years, and it changed my career. This unique and user friendly software will add many thousands to your income for as long as you’re in business. InsMark makes me look good, and it will you as well.”

Simon Singer, CFP®, CAP®, RFC®, Past President International Forum, InsMark Platinum Power Producer®, Encino, CA

“InsMark is the Picasso of the financial services world — their marketing savvy never fails to amaze me.”

Doug Peete, Past President, Top of the Table, InsMark Silver Power Producer®, Overland Park, KS

“The reason I use InsMark products is because they are so good at explaining financial concepts to all three parties: 1) the producer trying to explain the idea; 2) the computer technician trying to illustrate it; 3) the customer trying to understand it.”

Rich Linsday, CLU, AEP, ChFC®, InsMark Platinum Power Producer®, Top of the Table, International Forum, Pasadena, CA

“I really thought I knew all the sales techniques that affect my business, but I do now, thanks to InsMark.”

Sam Keck, MBA, CLU, CFP®, LUTCF, InsMark Platinum Power Producer®, Financial Planner, Denver, CO

“InsMark” and “Wealthy and Wise” are registered trademarks of InsMark, Inc.

“Documents On A Disk” is a trademark of InsMark, Inc.

Important Note #1: The hypothetical values associated with this Blog assume the nonguaranteed values shown continue in all years. This is not likely, and actual results may be more or less favorable. Life insurance illustrations are not valid unless accompanied by a basic illustration from the issuing life insurance company.

Important Note #2: The information in this Blog is for educational purposes only. In all cases, the approval of a client’s legal and tax advisers must be secured regarding the implementation or modification of any planning technique as well as the applicability and consequences of new cases, rulings, or legislation upon existing or impending plans.

Important Note #3: Many of you are rightly concerned about the potential tax bomb in life insurance that can accidentally be triggered by a careless policyowner when policy loans are present and net cash values are so low that the income tax on the gain on surrender (calculated using gross cash values less basis) is more – often significantly more – than the net cash surrender value.

This lurking tax bomb can be present in all forms of whole life and universal life where policy loans of any type are utilized. It can be avoided, and you, the producer, are key to making sure your clients are aware of how to sidestep it.

A tax bomb can be avoided if the policy is neither surrendered nor allowed to lapse, since the policy death benefit wipes away the income tax liability. The foundation of this special treatment is IRC Section 101. This statute provides that the proceeds of life insurance maturing as a death claim are exempt from federal income tax. This applies to the full death benefit, including any cash value component whether loans exist or not.

Can your clients remember these facts years into the future? If they are incapacitated, will family members understand the issues? It is probably best to file a short note with the policy – something like this (although your compliance officer will likely have preferred language):

If/when you take policy loans on this policy, be sure to talk to your financial adviser before surrendering or lapsing the policy in order to anticipate unexpected tax consequences that may otherwise be avoided.

Does this note make it harder or easier to deliver the policy? It’s harder if you haven’t discussed it with your client; easier if you have. And that’s the point – you should discuss it.

Some life insurance companies have concierge units that monitor loan status at the point of lapse or surrender, and you would be well-advised to select an insurance company with this capacity. To be effective regarding the tax bomb, such carriers need to be proactive in their client relationships, not merely reactive to client inquiries. I hope that ultimately the policyholder service division of all life insurance companies will bring this potential liability to the attention of those surrendering or lapsing policies, particularly those policies with 50% or more of the gross cash value subject to outstanding loans.