(Click here for Blog Archive)

(Click here for Blog Index)

(Presentations in this blog were created using the InsMark Illustration System and Wealthy and Wise®)

|

The basic life insurance illustration has lately become a compliance document. I saw one recently with 52 pages, some of which were close to incomprehensible. Part of the problem is that the basic illustration must serve too many masters: legal, actuarial, sales, and, often excluded, artistic. Fortunately, InsMark’s supplemental illustrations deal only with sales and artistic.

When you include supplemental illustrations in your presentation, such as those provided by InsMark, which of the following do you – or more particularly, your client – find desirable?

- Just the Facts?

- Facts with Limited Backup?

- Facts with Serious Backup?

- Facts with Intense Backup?

Deciding just how much information you want to convey to a prospective client requires some serious thought. The decision is typically based on your and your prospect’s comfort zone which are not always in sync.

Let’s take the case of Brad and Ann Parker, both age 35, and a referral from a current client. Following up from your fact-finding meeting with the Parkers, you intend to present an illustration insuring Brad for $600,000 of max-funded Indexed Universal Life (“IUL”). You’re not sure to what extent they may want to consider alternatives, or will they likely want to think about term insurance, i.e., how much will folks like Suze Orman and Dave Ramsey have influenced their thinking? You will definitely want to have “just in case” illustrations available that address these issues.

Just the Facts

This presentation strategy involves a composite of three key illustrations from the InsMark Illustration System, any one of which might do the job, but in tandem, the combination can be seriously convincing. We call this Checkmate Selling® because it involves answering objections before they surface as part of the presentation process. Each of the three illustrations contains the identical policy data sourced from the carrier’s basic illustration system, and each is coupled with an informative graphic.

The three illustrations are:

- Life Plan

- Various Financial Alternatives

- Permanent vs. Term

Click here to view Just the Facts – a total of 7 pages.

Facts with Limited Backup

Maybe you want a little more detail, and this variation adds some graphics. (Notice on the Life Plan line graph that both the cash value and death benefit rates of return exceed 8.00% at year 60. How can this be with IUL illustrated at 7.00%? It is due to the extraordinary financial firepower of participating loans.)

Note: In the other two illustrations, a pre-tax equivalent rate is reflected on the Matching Values report. If you want these to show the net equivalent rate, you can do so under Options/Preferences/Report Preferences on the Workbook Main Window.

Click here to view Facts with Limited Backup – a total of 14 pages.

Facts with Serious Backup

|

This variation provides the full enchilada: Cover Page, Table of Contents, Section Pages, extensive numerical backup, and several text pages of important information. Click here to view Facts with Serious Backup – a total of 38 pages. Some may think that “Just the Facts” is OK as is. How about Brad and Ann – is it OK for them too? It’s important that you are comfortable with the material, but be sure to consider their perspective as well. Many believe that the addition of graphics in “Facts with Limited Backup” adds a compelling feature that will be appreciated by most prospects. Some may prefer “Facts with Serious Backup” and welcome its detail. Or will it overwhelm Brad and Ann? One advantage of this variation: it provides important related material should they ask their CPA or attorney to review it. I think it adds to your professionalism to have it available. You can always skip some of the more involved reports. |

|

Suggestion: Bring all variations with you to the interview. Start with “Just the Facts”, and introduce the other ones as appropriate.

Facts with Intense Backup

If, for example, your presentation is to a savvy investor or maybe an engineer or a CPA, there is an even more thorough evaluation resource. This involves a comprehensive analysis of a current retirement plan compared to a revision that includes a significant amount of cash value life insurance. Our Wealthy and Wise® System is the perfect analytical tool for a “do it vs. don’t do it” assessment like this. I did this in Blog #58: A New Retirement Planning Strategy. If this approach interests you, I recommend you study this Blog.

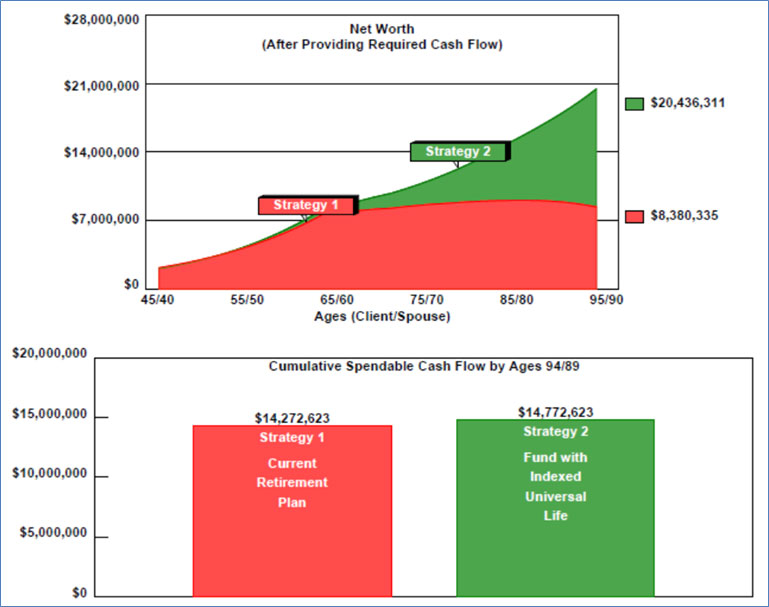

Let me provide you with an example of “Facts with Intense Backup” that is featured in Blog #58 referenced above that has to do with generating maximum cash flow at retirement. In it, five $100,000 premiums are used to purchase $2,500,000 of max-funded IUL for Tony Callahan, age 45. The premiums are funded from current assets not out-of-pocket dollars. Below is the resulting graphic showing the impact on net worth and retirement cash flow for Tony and his wife, Jennifer, age 40.

| Image 1 |

| Strategy 1: Current Plan |

| vs. |

| Strategy 2: Add IUL to Current Plan |

Strategy 2 shows a long-range increase in net worth in excess of $12,000,000 (an increase of 143%). The gain in net worth of Strategy 2 is caused primarily by the substantial participating policy loans from the IUL which significantly reduce the amount of cash flow needed from other assets. Be sure you understand that the only difference between the two strategies is the inclusion of IUL in Strategy 2. In all other respects, they both reflect the identical data.

In the lower half of the graphic, you can see that both strategies produce more than $14,000,000 in spendable retirement cash flow. $9,000,000 of that is $300,000 a year times 30 years (ages 65/60 through ages 95/90). The balance is the result of the 3.00% indexing.

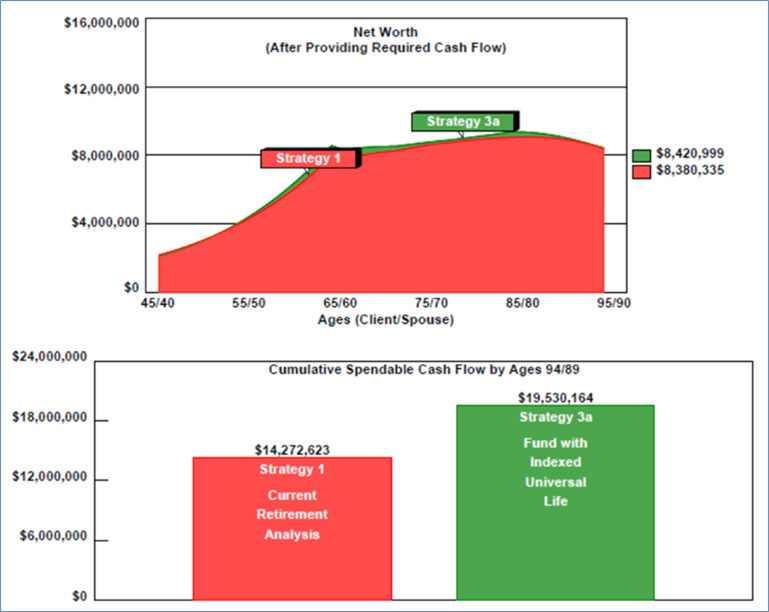

Next, Blog #58 illustrates a significant increase in spendable cash flow in Strategy 3a.

| Image 2 |

| Strategy 1: Current Plan |

| vs. |

| Strategy 3a: Current Plan + IUL + More Cash Flow |

Strategy 3a provides an additional $100,000 a year indexed at 3.00% starting at age 65 while reducing long-range net worth to $8,420,999, virtually identical to the long-range net worth Strategy 1 of $8,380,335, the Callahan’s current plan.

For those of you specializing in retirement cash flow from cash value life insurance, this unique use of our Wealthy and Wise retirement and estate planning system can put you head and shoulders above your competition by providing either an increase in net worth or spendable cash flow (or some of each). You don’t want a competitor showing this logic to your prospects and clients.

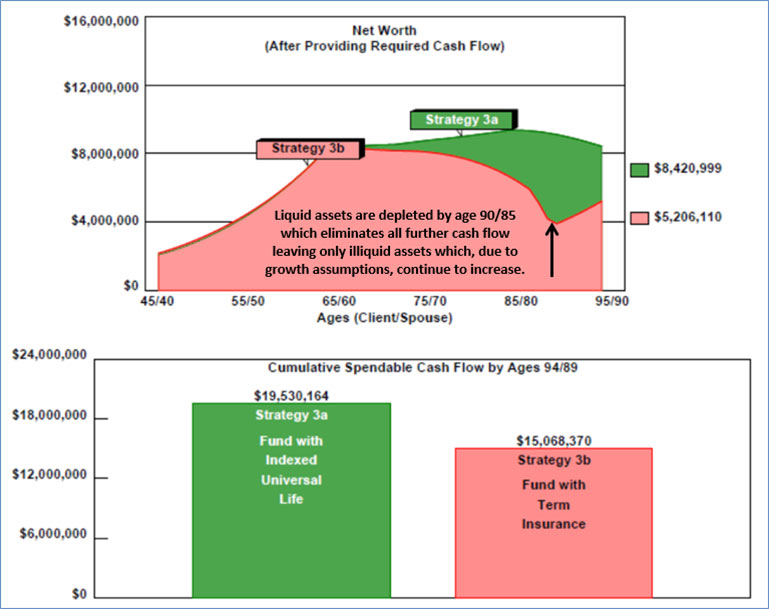

The comparison ends by introducing Strategy 3b in which $2,500,000 of inexpensive 20-year level term insurance is used instead of IUL causing Strategy 3b to collapse.

| Image 3 |

| Strategy 3a: Current Plan + IUL + More Cash Flow |

| vs. |

| Strategy 3b: Current Plan + Term + More Cash Flow |

Thoughts on Term Insurance

I have often been asked by our users if I really think term insurance should be introduced without a prospect first bringing it up? I do because you never know when a prospect will ask his CPA, a family friend, or a brother-in-law for an opinion when you aren’t present, or will come across a TV or radio show by Suze Orman or Dave Ramsey. What kind of answer do you think will surface from them? It won’t be “buy cash value insurance.”

I believe you can educate prospects as to the pitfalls of term insurance as part of the presentation process so they are informed in advance of its significant disadvantages.

Conclusion

I know that many of my readers are comfortable selling the retirement cash flow features of IUL using a stand-alone illustration that is not integrated with a client’s other assets, and that is why I began this Blog with three examples of effective ways to do that.

Clients typically consider the premiums to be an expense for such plans. Changing to a Wealthy and Wise analysis creates a new learning curve because your presentation changes to asset transfer.

|

Believe this: the wealthier a client, the easier it is to convince him or her of the power of integrating IUL into their portfolio of assets. With allocations from current assets as the source of the IUL premiums as shown in Blog #58, it becomes a case of “comparing assets and cash flow if you do it -- with what happens if you don’t”. That is a completely different presentation, and it can have compelling results for you. With some clients, Strategy 2 (greater net worth) will be sufficient; others will be very impressed (perhaps even astonished) with Strategy 3a logic (greater cash flow) -- or, perhaps, the best solution involves some of each one. |

|

The payoff? You will develop much higher average compensation per case, and a client locked into your planning expertise, not just an IUL policyholder. Tended carefully, you will likely have this client for life.

If you are an experienced user with Wealthy and Wise, putting a case together like this, although detailed, will be relatively straightforward. (Blog #58 provides you with access to the digital Workbook I used to prepare those presentations.)

That’s the good news. The bad news for some is that you have to gather all of your client’s financial data for a Wealthy and Wise analysis. Many of my readers are used to doing this. For those of you who are not so comfortable with it, how do feel about asking a prospective client to reveal full details of financial data? Clearly, you must earn a prospective client’s trust to do that. My suggestion for the best way to gain that confidence is to share examples of how this concept works for others using Blog #58 and the Wealthy and Wise reports associated with it.

Note: A Fact Finder is available in Wealthy and Wise to guide you in your data gathering (see Tools on the main menu bar). Many of our licensees tell me they think the Fact Finder is best filled out with the client(s) present and involved in the process.

At first glance the Fact Finder may look intimidating, but on most pages, you will be entering data in only a few of the listed categories. To acquaint yourself with it, try filling one out for your own situation. Then enter your data in your Wealthy and Wise System -- you will be pleasantly surprised.

InsMark’s Digital Workbook Files

If you would like some help creating customized versions of the presentations in this Blog for your clients, watch the video below on how to download and use InsMark’s Digital Workbook Files.

New Zip File Downloaders

Watch the video.

Experienced Zip File Downloaders Download the zip file, open it, and double click the Workbook file name to open it in your InsMark System.

|

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark System. Please forward the Workbook where you can launch it on your PC where your InsMark System(s) are installed. |

If you obtain the digital workbook for Blog #162, click here for a guide to its content.

Licensing InsMark Systems

To license any of the InsMark software products, visit our Product Center online or contact Julie Nayeri at Julien@insmark.com or 888-InsMark (467-6275). Institutional inquiries should be directed to David Grant, Senior Vice President — Sales, at dag@insmark.com or (925) 543-0513.

For help on how to use InsMark software, go to The Quickest Way To Learn InsMark.

Testimonials

“InsMark’s Checkmate Selling® strategy is still one of the most compelling tools to bring a client to a definitive decision, based on their best case alternatives!!! Solid mathematical comparisons that prove the validity of our insurance solution!!!”

Frank Dunaway, III, CLU, Legacy Advisory Services, Carthage, MO

“InsMark’s Life Plan presentation provides a valuable tool for our agents in discussing retirement plans with their clients. Its concise and to-the-point design makes the concept very easy to understand. And, having it available in both Spanish and English has proven to be extremely useful.”

Zerita Reynolds, CLU, ChFC, FLMI, LLIF, REBC, RHU Director, Advanced Markets, Aviva USA

“InsMark is the Picasso of the financial services world – their marketing savvy never fails to amaze me.”

Doug Peete, Past President, Top of the Table, InsMark Power Producer®, Overland Park, KS

“The InsMark software is indispensable to my entire planning process because it enables me to show my clients that inaction has a price tag. I can’t afford to go without it!”

David McKnight, Author of The Power of Zero, InsMark Power Producer®, Grafton, WI

“The InsMark Illustration System and Wealthy and Wise have significantly enhanced my life insurance production scope. I feel I can now present ideas with backup support material.”

Ross Hoffman, Ventura, CA

Important Note #1: The hypothetical life insurance illustration associated with this Blog assumes the nonguaranteed values shown continue in all years. This is not likely, and actual results may be more or less favorable. Actual illustrations are not valid unless accompanied by a basic illustration from the issuing life insurance company.

Important Note #2: Many of you are rightly concerned about the potential tax bomb in life insurance that can accidentally be triggered by a careless policyowner. Click here to read Blog #51: Avoiding the Tax Bomb in Life Insurance.

Important Note #3: The information in this Blog is for educational purposes only. In all cases, the approval of a client’s legal and tax advisers must be secured regarding the implementation or modification of any planning technique as well as the applicability and consequences of new cases, rulings, or legislation upon existing or impending plans.

“InsMark”, “Wealthy and Wise”, and “CheckMate Selling” are registered trademarks of InsMark, Inc.