(Click here for Blog Archive)

(Click here for Blog Index)

(Presentations in this blog were created using the InsMark Illustration System)

|

Jennifer Hunt, age 40, is President and sole shareholder of Midland Oil Supply, Inc., a successful S corporation with 50 employees. She is in a 40% income tax bracket. Her adviser has suggested she consider installing a Profit Sharing Plan (“PSP”).

“There are too many employees I’d have to cover,” she replies. “Besides, we already have a generous 401(k) plan.”

The adviser continues, “If you could do a deductible retirement plan just for yourself, how much would you contribute?”

“Deductible? Six figures probably -- maybe $250,000.”

Case Study of a Powerful Alternative

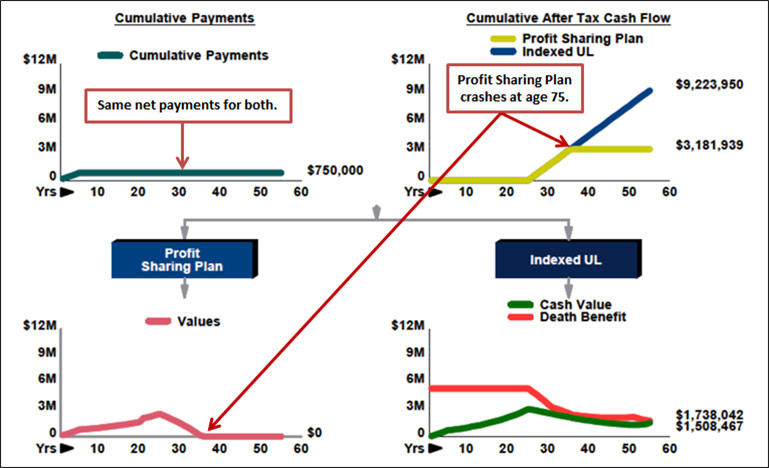

$250,000 a year for five years paid into a hypothetical deductible PSP just for Jennifer costs her $150,000 in her 40% income tax bracket, a total of $750,000.

Tax Calculation: Each year for five years, the deduction of $250,000 for the PSP flows to Jennifer personally (don’t forget Midland Oil Supply is an S corporation). She realizes a tax savings each year on her personal return of $100,000 (40% of $250,000). Midland Oil spends $250,000 for the PSP each year, and Jennifer saves $100,000 each year equaling a combined net cost of $150,000 each year ($250,000 minus $100,000). Assume a 7.00% yield on the funds in the PSP.

Alternative Tax Calculation: Instead of Midland Oil Supply spending $250,000 each year for five years on the hypothetical PSP, the company distributes those same funds to Jennifer. She pays $100,000 of income tax each year leaving her with $150,000 which she uses for premiums for a personally-owned Indexed Universal Life (“IUL”) illustrated at the same 7.00%.

Note: Both sets of calculations would be identical if Midland Oil Supply were a Limited Liability Company.

Retirement is assumed to occur at Jennifer’s age 65 where the IUL is illustrated producing annual, spendable, retirement cash flow of $307,465 using participating policy loans. The PSP is illustrated producing the identical spendable cash flow of $307,465; however, as you can see below, it unfortunately runs out of funds at Jennifer’s age 75.

| Profit Sharing Plan vs. Indexed Universal Life |

| (Image 1) |

Click here to review the comparative reports for this Case Study prepared using the Other investments vs. Your Policy module in the InsMark Illustration System. The difference is substantial as the IUL produces more than $6 million in additional spendable cash flow than the PSP. The PSP is exhausted by Jennifer’s age 75.

Alternative PSP

In order for the cash flow of the PSP to last for as many years as the IUL, Jennifer could withdraw an annual level amount of $270,843. After tax, this would provide her with spendable cash flow of $162,506, a 47% reduction from the spendable cash flow of the $307,465 provided by the IUL. The PSP is exhausted at her age 95 compared to the cash value of the IUL at age 95 of $1,508,467 wrapped up in $1,738,042 of death benefit.

Click here for the illustration of this alternative PSP using the Defined Contribution Retirement Plan module available on the InsCalc® tab in the InsMark Illustration System.

Sequential Funding of Additional IUL

Jennifer is age 40 – why illustrate only five years of funding? Safety valve reasons . . . Jennifer may decide to sell the business, and she likely won’t want to be tied to a multi-year, pre-retirement plan. After five years, if Midland Oil Supply continues under her ownership, she should do another IUL on the same basis – and maybe another one five years after that.

Conclusion

The PSP is not a close financial competitor.

Additional differences are:

- Unlike the PSP, tax free cash flow from the IUL can be accessed prior to age 59 1/2 with no 10% premature distribution tax.

- Unlike the PSP, the IUL provides a significant pre-retirement death benefit for Jennifer’s family.

- Unlike the PSP, a waiver of premium can be attached to the IUL in the event of disability.

- In the event, income taxes increase during Jennifer’s retirement as a result of dealing with a runaway federal deficit, cash flow from the PSP will be seriously impacted; the IUL will be unaffected.

InsMark’s Digital Workbook Files

If you would like some help creating customized versions of the presentations in this Blog for your clients, watch the video below on how to download and use InsMark’s Digital Workbook Files.

New Zip File Downloaders

Watch the video.

Experienced Zip File Downloaders Download the zip file, open it, and double click the Workbook file name to open it in your InsMark System.

|

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark System. Please forward the Workbook where you can launch it on your PC where your InsMark System(s) are installed. |

If you obtain the digital workbook for Blog #154, Click here for a guide to its content.

Licensing InsMark Systems

To license any of the InsMark software products, visit our Product Center online or contact Julie Nayeri at Julien@insmark.com or 888-InsMark (467-6275). Institutional inquiries should be directed to David Grant, Senior Vice President – Sales, at dag@insmark.com or (925) 543-0513.

For help on how to use InsMark software, go to The Quickest Way To Learn InsMark.

Testimonials

“The InsMark software is indispensable to my entire planning process because it enables me to show my clients that inaction has a price tag. I can’t afford to go without it!”

David McKnight, Author of The Power of Zero, InsMark Gold Power Producer®, Grafton, WI

“The reason I use InsMark products is because they are so good at explaining financial concepts to all three parties: 1) the producer trying to explain the idea; 2) the computer technician trying to illustrate it; 3) the customer trying to understand it.”

Rich Linsday, CLU, AEP, ChFC, InsMark Power Producer®, Top of the Table, International Forum, Pasadena, CA

“InsMark’s Checkmate® Selling strategy is still one of the most compelling tools to bring a client to a definitive decision, based on their best case alternatives!!! Solid mathematical comparisons that prove the validity of our insurance solution!!!”

Frank Dunaway, III, CLU, Legacy Advisory Services, Carthage, MO

Important Note #1: The hypothetical life insurance illustration associated with this Blog assumes the nonguaranteed values shown continue in all years. This is not likely, and actual results may be more or less favorable. Actual illustrations are not valid unless accompanied by a basic illustration from the issuing life insurance company.

Important Note #2: Many of you are rightly concerned about the potential tax bomb in life insurance that can accidentally be triggered by a careless policyowner. Click here to read Blog #51: Avoiding the Tax Bomb in Life Insurance.

Important Note #3: The information in this Blog is for educational purposes only. In all cases, the approval of a client’s legal and tax advisers must be secured regarding the implementation or modification of any planning technique as well as the applicability and consequences of new cases, rulings, or legislation upon existing or impending plans.