(Click here for Blog Archive)

(Click here for Blog Index)

(Presentations in this blog were created using the InsMark Illustration System

|

Note from Bob: “Best policy for my client” cannot be established by a standard that applies to all clients. Rather, it must be determined by an objective analysis that is unique to each client as to the type of policy as well as each client’s personal comfort with different levels of death benefit, cash value, cash flow, and interest or dividend assumptions. This week we have a guest Blog presented by Brian Manderscheid, Vice President and Advanced Case Designer for LifePro Financial Services, Inc., San Diego, CA, that addresses these critical issues featuring InsMark Compare, our new spreadsheet module that compares various policy types and benefits. |

Bob - as we discussed last week, we have had a lot of success with the InsMark Compare report in the InsMark Illustration System. Specifically, we are able to help our agents work with their clients in more of an advisory role and less as a salesman or ‘product pusher.’ The InsMark Compare report is very timely due to the new Department of Labor (DOL) ruling on fiduciary standards and best interest contracts pertaining to retirement advice.

Bob - as we discussed last week, we have had a lot of success with the InsMark Compare report in the InsMark Illustration System. Specifically, we are able to help our agents work with their clients in more of an advisory role and less as a salesman or ‘product pusher.’ The InsMark Compare report is very timely due to the new Department of Labor (DOL) ruling on fiduciary standards and best interest contracts pertaining to retirement advice.

While this new ruling will most likely affect advisors who work in the rollover market, it may also prompt a shift in how financial products in general are sold.

My idea for this Blog is to help show the power of the InsMark Compare report but also help advisors avoid the ‘product pusher salesman’ trap. By offering non-biased advice based on what’s best for the client, our advisors are able to ‘sell’ more insurance than most other groups. Additionally, this level of service produces more referred leads than the salesman type approach which is mostly transactional.

Below, I broke down three advisory-type sales methods using the InsMark Compare report.

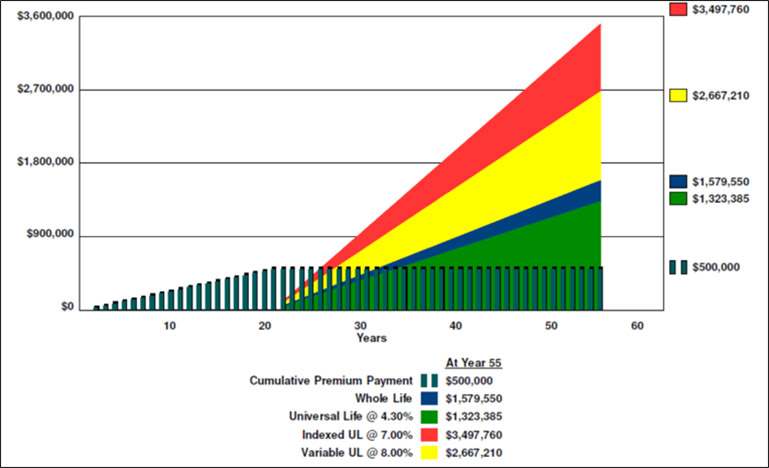

Proposal #1 - Risk Spectrum

Rather than lumping every client who walks in the door as someone who should buy a specific product, we can match up our product offerings to each of our prospects individual level of risk. The InsMark Compare report allows us to illustrate up to 4 different product types side by side in a customizable, comprehensive, yet easy to understand report. This allows us to present products from the most conservative Whole Life to the most aggressive Variable Universal Life and, of course, products in-between.

Below is one of the InsMark Compare graphics from this analysis:

| Image 1 |

| Proposal #1 - Risk Spectrum |

| Summary Analysis of |

| Cumulative After Tax Loan Proceeds |

Click here to review the entire InsMark Compare report for Proposal #1 - Risk Spectrum.

In addition to the full report, InsMark provides a comprehensive risk questionnaire from Back Room Technician (Advisys) that can be used in a pre-appointment conversation in order to determine your prospect’s risk tolerance. Once we have determined our prospect’s level of risk, we can then match up the product that best matches their risk tolerance. For example, a prospect with a Moderate to Moderately Aggressive risk tolerance may be best suited for Indexed Universal Life rather than a more conservative Whole Life.

Note for advisors who aren’t securities-licensed: The Variable Universal Life illustration can be eliminated from any InsMark Compare evaluation. Other products such as Guaranteed Universal Life, Guaranteed Indexed Universal Life or Non-Participating or Interest Sensitive Whole Life could be added and located on the left side of the illustration in a Conservative risk tolerance category.

Proposal #2 - Carrier Compare

After determining the appropriate product type for our prospect, we can then move to a carrier comparison. Using the InsMark Compare report we can contrast up to 4 different carriers side by side rather than sifting through 4 carrier proposals (upwards of 40 pages each). We can compare certain variables such as illustrated rates as well as performance measures such as cash value, income and death benefit. In our example our prospect’s risk tolerance from Backroom Technician matches up best to Indexed Universal Life. We then hand-selected 4 carriers that offer very competitive IULs to show the client we did our due diligence in carrier selection. Again, this helps our agent act in an advisory role rather than pushing one specific carrier.

Below is one of the InsMark Compare graphics from this analysis:

| Image 2 |

| Proposal #2 - Carrier Compare |

| Summary Analysis of |

| Cumulative After Tax Loan Proceeds |

Click here to review the entire InsMark Compare report for Proposal #2 - Carrier Compare.

As you can see in this InsMark Compare report, ‘Carrier A’ provides the highest illustrated income even though it has the 3rd lowest Actuarial Guide 49 (AG49) illustrated rate. With discussion of additional important variables such as loan rates, indexed crediting strategies, interest rate bonuses, carrier financials and renewal rates, we were able to narrow down ‘Carrier A’ as the best product for our prospect.

Note: This report was run at each carrier’s AG49 rate to take into consideration each carrier’s current cap rates. It can be modified to show each carrier earning the same illustrated rate such as 6% or 7% (depending upon each carrier’s AG49 rate).

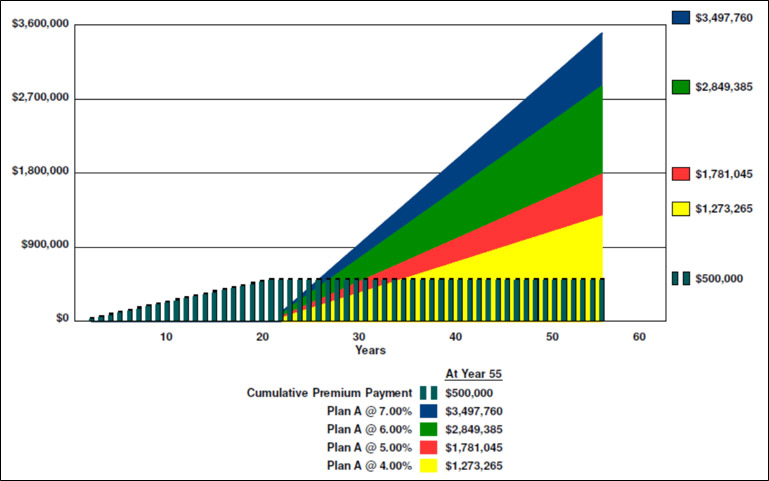

Proposal #3 - Illustrated Rates

Far too many times we’ve seen agents try to prove or justify high illustrated rates to their prospects and lose sales as a result. While AG49 has helped minimize ‘too good to be true’ illustrations, some agents still illustrate at the maximum rates and argue there is no way the product will perform any less. To avoid this salesman trap, we can again use InsMark Compare to provide the client with a range of illustrated performance. Showing the client 4 separate carrier illustrations may not only be cumbersome, it can also prove to be a waste of paper. In this example, we illustrated IUL ‘Carrier A’ at 4 different illustrated rates of 7%, 6%, 5%, and 4%. At these rates the projected tax free retirement income ranges from a low of $36,379 to a high of $99,936. While just shy of six figures of annual tax free income looks the most enticing, our clients need to understand past performance is no guarantee of future results. Providing the client a range of performance demonstrates your credentials as a trusted adviser, it also helps reduce any potential future liability from claims such as “I didn’t know the cash flow from the policy could be less than illustrated”.

Below is one of the InsMark Compare graphics from this analysis:

| Image 3 |

| Proposal #3 - Illustrated Rates |

| Summary Analysis of |

| Cumulative After Tax Loan Proceeds |

Click here to review the entire InsMark Compare report for Proposal #3 - Illustrated Rates.

This InsMark Compare report can also be run with the same income for each illustrated rate but with shorter income durations for lower rates. While the $99,936 illustrated income will last to age 100 with a 7% illustrated rate, it may only last to age 72 at a 4% illustrated rate.

In addition to providing valuable advisory process on how to sell more life insurance, there are several other great uses of the InsMark Compare report:

- Comparing different face amounts or price points with the same product or multiple products;

- Comparing different premium funding amounts, funding options or funding durations with the same product or multiple products;

- Comparing taking income from an IUL at different ages such as 62, 66, 70 and 75;

- Comparing single life products on each spouse vs. a survivorship life;

- Comparing a premium financed program vs. a non-financed program.

Conclusion

With the power of the InsMark software system and the techniques outlined above, you can become your prospects trusted advisor, increase referrals, and just about eliminate any competition. Likewise, with the fiduciary standards imposed by DOL on retirement advice, the InsMark Compare report ensures you are not only providing suitable advice but also offering the best products available. While the reach of the DOL ruling may not be fully understood, it is important that as advisors we start to shift our focus from product selling to offering trusted advice.

Licensing InsMark Systems

To license the InsMark Illustration System, visit InsMark online or contact Julie Nayeri at julien@insmark.com or 888-InsMark (467-6275). Institutional inquiries should be directed to David Grant, Senior Vice President - Sales, at dag@insmark.com or (925) 543-0513.

InsMark’s Digital Workbook Files

If you would like some help creating customized versions of the presentations in this Blog for your clients, watch the video below on how to download and use InsMark’s Digital Workbook Files.

Digital Workbook Files For This Blog

Download all workbook files for all blogs

|

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark System. Please forward the Workbook where you can launch it on your PC where your InsMark System(s) are installed. |

Testimonials

“I really thought I knew all the sales techniques that affect my business, but I do now, thanks to InsMark.”

Sam Keck, MBA, CLU, CFP, LUTCF, InsMark Platinum Power Producer®, Financial Planner, Denver, CO

“InsMark provides incredible tools to give clients a visual of how they can optimize their wealth. It’s great for deciding which road to go down.”

Jim Heafner, MBA, CFP, Heafner Financial Solutions, Inc., Charlotte, NC

“InsMark’s Checkmate® Selling strategy is still one of the most compelling tools to bring a client to a definitive decision, based on their best case alternatives!!! Solid mathematical comparisons that prove the validity of our insurance solution!!!”

Frank Dunaway, III, CLU, Legacy Advisory Services, Carthage, MO

Important Note #1: The hypothetical values associated with this Blog assume the nonguaranteed values shown continue in all years. This is not likely, and actual results may be more or less favorable.

Important Note #2: Many of you are rightly concerned about the potential tax bomb in life insurance that can accidentally be triggered by a careless policyowner. Click here to read Blog #51: Avoiding the Tax Bomb in Life Insurance.

Important Note #3: The information in this Blog is for educational purposes only. In all cases, the approval of a client’s legal and tax advisers must be secured regarding the implementation or modification of any planning technique as well as the applicability and consequences of new cases, rulings, or legislation upon existing or impending plans.