My last three Blogs (#96, #97, and #98) dealt with Premium Financing integrated with Wealthy and Wise, our wealth planning system. With that, I thought I was done with premium financing for a while. But over the weekend, one of our licensees told me his client’s CPA had reviewed one of his premium financing illustrations and pooh-poohed it by saying, “This is way too complicated. Why not just take the cost of the premium financing and invest in some equities.”

That’s an unsophisticated, although not uncommon, objection to cash value life insurance in general. So let’s see what happens if we compare a hypothetical equity account alternative to the premium financing case examined in Blog #98.

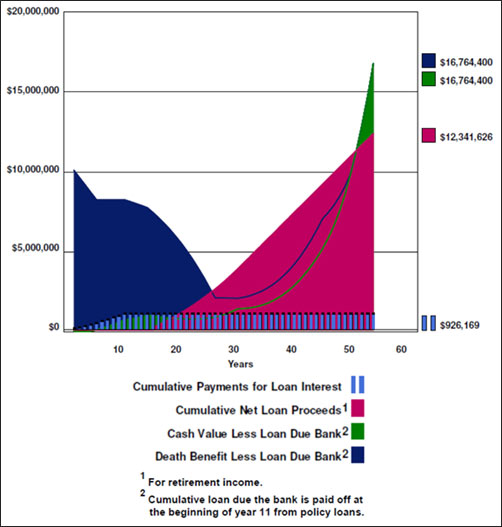

Here again are the results of the premium financing case using Indexed Universal Life (IUL):

| Graphic from the Premium Financing Illustration |

| Robert Sullivan, Age 46 |

Click here to review the full illustration.

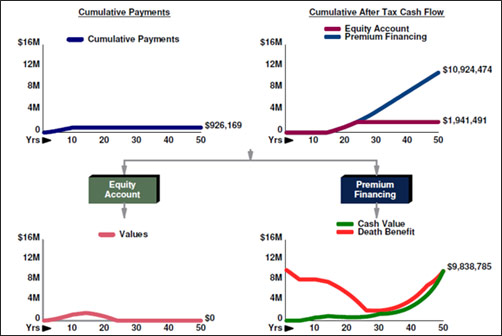

Next, we’ll compare the cost of the premium financing illustration with an equity account using a growth rate of 7.50% (similar to the IUL interest rate used in the premium financing) plus a 2.50% dividend assumption for a total presumed yield of 10.00%.

Below is a graphic of the results from the Other Investments vs. Your Policy module in the InsMark Illustration System using the cost of the premium financing as the alternative deposit to the equity account.

Click here to review the full comparative illustration.

The results in favor of the premium financing are remarkable. As you can see in the upper right quadrant of the graphic above, the gain in after tax retirement cash flow is almost $9 million. And on the lower right, there is also almost $10 million of cash value in the premium financing instead of $0 in the equity account.

All this for the same payments into either plan of $926,169!

Over the years illustrated, the equity account would have to have a growth rate 15.55% plus the assumed dividend of 2.50% (total 18.05%) to match the overall results of the premium financing. That’s 241% greater that the interest rate of 7.50% assumed for the IUL. This clearly dismisses any convincing argument that IUL participation rates in the S&P don’t account for dividends. They don’t need to! It’s no wonder several big mutual companies recently tried to deliver a knockout blow to IUL. Was it in the name of consumer protection as they claimed? Hardly -- it was due to critical competitive pressure on whole life.

This favorable result is not applicable merely to a comparison to an equity account. It applies to virtually any comparison of a reasonable alternative to the IUL/premium financing combination. For example, it would take a yield of 24.20% on a taxable account and 14.79% on an indexed tax deferred annuity to match the results of the premium financing (with zero life insurance protection). If you want the System Workbook files associated with this Blog (see below), included is an illustration from the Various Financial Alternatives module in the InsMark Illustration System with precisely these results.

Note: It doesn’t take a premium financing analysis to bury an equity account (or a taxable or tax deferred account). A max-funded IUL will do the job -- every time.

Conclusion

Most clients make the best decisions using comparisons, and you can’t counter the objection “Life insurance is a lousy investment” using just the basic illustration. There is no economic theory that explains why a bad idea is acceptable just because you hear it frequently. If you have the cash flow to buy what you want, cash value life insurance is the only logical choice. InsMark can help you prove it.

Below is a quote from a terrific article in the December 2014 issue of Trusts & Estates by Bill Boersma in which he discusses life insurance as an asset class:

“I can only wonder if another asset with the same qualities would be implemented more frequently if it wasn’t called life insurance.”

Does all this convince you to include premium financing in your offerings to upscale clients? It is not intended to unless it fits your comfort zone and your client base. If nothing else, I hope my remarks emphasize the extraordinary power of IUL no matter in what context it is presented.

Details of the Equity Account Calculations

I assumed a capital gains and dividend tax rate of 30% (including a provision for state tax). I assumed a 30% turnover ratio and 60% of the growth would be subject to long-term gains; 40% short-term gains. The Sullivans’ 45% income tax bracket was also included.

I also used a 1.50% management fee. Too high? Too low? Ask a dozen experts and you’ll get varied opinions. In next week’s Blog #100, I’ll have some details on management fees -- the results will likely surprise you.

InsMark’s Digital Workbook Files

If you would like some help creating customized versions of the presentations in this Blog for your clients, watch the video below on how to download and use InsMark’s Digital Workbook Files.

Digital Workbook Files For This Blog

Download all workbook files for all blogs

|

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark System. Please forward the Workbook where you can launch it on your PC where your InsMark System(s) are installed. |

Licensing InsMark Systems

To license the Premium Financing System and/or the InsMark Illustration System, contact Julie Nayeri at julien@insmark.com or 888-InsMark (467-6275). Institutional inquiries should be directed to David Grant, Senior Vice President ? Sales, at dag@insmark.com or (925) 543-0513.

Testimonials:

“Standard premium financing illustrations produce much in the way of great data, but it takes the InsMark Premium Financing System to really present compelling numbers; however, the integration of that data into InsMark’s comparative modules like Various Financial Alternatives and Wealthy and Wise is really what makes premium financing sizzle.”

Chris Jacob, CFP, SFI-Cadeau, St. Louis, MO, InsMark Platinum Power Producer®

“The InsMark software is indispensable to my entire planning process because it enables me to show my clients that inaction has a price tag. I can't afford to go without it!”

David McKnight, Author of The Power of Zero, Grafton, WI, InsMark Gold Power Producer®

Important Note #1: This information in this Blog and any referred material is for educational purposes only. In all cases, the approval of a client’s legal and tax advisers must be secured regarding the implementation or modification of any planning technique as well as the applicability and consequences of new cases, rulings, or legislation upon existing or impending plans.

Important Note #2: The hypothetical life insurance illustrations associated with this Blog assume the nonguaranteed values shown continue in all years. This is not likely, and actual results may be more or less favorable. Actual illustrations are not valid unless accompanied by a basic illustration from the issuing life insurance company.