David Wolfe, a neighbor of mine, is a very successful attorney. He is making maximum contributions to his law firm’s 401(k) plan.

Recently we were grilling steaks together, and got to talking about his 401(k). ?I asked him, “If you could put more into your 401(k), would you?”

His response was, “I would.”

I asked him, “How much?”

He thought for a moment, “$50,000 for sure; maybe more.”

Case Study

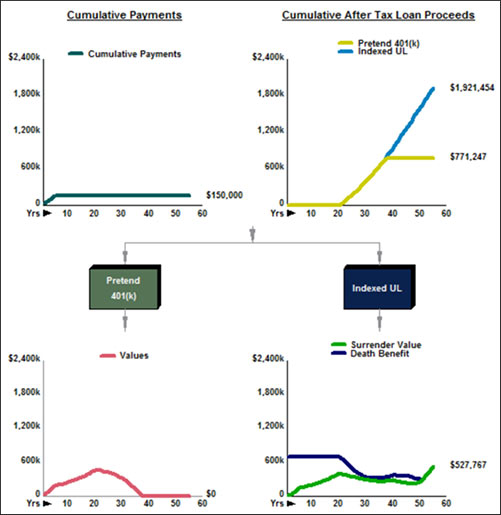

Let’s make believe for a moment that he can do it. We will illustrate David contributing $50,000 a year for the next five years to his pretend 401(k) plan. ? In his 40% marginal tax bracket, it costs him $30,000 each year after deducting his income tax savings ($50,000 - $20,000). We will compare the results to an Indexed Universal Life Policy (IUL) with scheduled premiums of $30,000 a year for five years, the same dollars as the after cost of his pretend 401(k) plan. ?We will illustrate both plans at 7.50%.

At age 65, we show David making tax free loans on the life insurance policy using an indexed schedule of participating loans starting with $33,000 and ending with $65,542 at age 99. ?We illustrated withdrawals on the pretend 401(k) plan that, after tax, match the same cash flow as the IUL.

There is no way the pretend 401(k) plan can compete with the IUL. ?Check out the InsMark graphic of the comparison below.

A Pretend 401(k) Plan vs. Indexed Universal Life

A Look at Year 55

Would you rather view trend lines?

Below is a summary of the two strategies:

|

|---|

|

|---|

Click here to review all the reports for this comparison from the InsMark Illustration System.

Additional Advantages

Unlike the pretend 401(k) plan, the IUL has four additional advantages:

- It provides a $700,000 life insurance death benefit;

- If the selected market index drops, there is no loss to the policy owner;

- There are no required minimum distributions;

- There is no 10% penalty tax associated for distributions prior to age 59?.

Conclusion

If you are a fan of Indexed Universal Life, there is no more powerful sales strategy I can suggest to you than the comparison between a pretend 401(k) plan and a life insurance policy. ?If you use it, you will never run out of prospective customers.

Prospecting

Imagine the response you would get if you ask the following question of individuals similar to David Wolfe:

“If you could invest an unlimited amount into your 401(k), how much more would you contribute annually over the next five years?”

Or this slight variation for those with no access at all to a 401(k):

“If you could invest an unlimited amount into a 401(k), how much would you contribute annually over the next five years?”

Either of these questions produces very favorable responses. When they occur, use the Other Investments vs. Your Policy in the InsMark Illustration System to show the results your policy vs. the pretend 401(k) plan.

Note: For those who are currently contributing to 401(k) plans in excess of the employer’s match, using life insurance as an alternative is also very effective for the portion that is not matched. See my Blog #61 - Sacrificing Cash Flow with a 401(k) Plan for details.

Note: Most owners of S Corporations, LLCs, or partners in Partnerships are well aware that their pass-through entities offer little opportunity for significant benefit plans. They typically have 401(k) plans with the standard limit on contributions -- like David Wolfe’s law firm. ?Introduce these individuals to a pretend 401(k) vs. IUL for as much excess contributions as they desire -- you’ll be well rewarded for the effort.

Why only five years of payments? ?It is a short time horizon which makes it easier for your prospect to decide. ?At the end of five years, do another one. And then another.

Important Note: ?Many of you are rightly concerned about the potential tax bomb in life insurance that can accidentally be triggered by a careless policyowner. ?Click here to read Blog #51: Avoiding the Tax Bomb in Life Insurance.

InsMark’s Digital Workbook Files

If you would like some help creating customized versions of the presentations in this Blog for your clients, watch the video below on how to download and use InsMark’s Digital Workbook Files.

Digital Workbook Files For This Blog

Download all workbook files for all blogs

|

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark System. Please forward the Workbook where you can launch it on your PC where your InsMark System(s) are installed. |

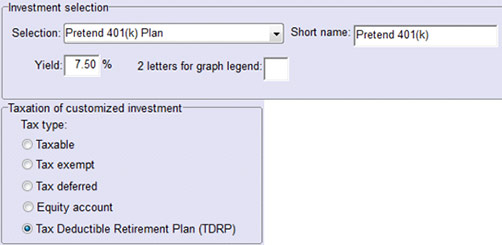

Note: On the Investment selection tab in the System Workbook, I used a “customize” selection as shown below:

Licensing

To license the InsMark Illustration System, contact Julie Nayeri at julien@insmark.com or 888-InsMark (467-6275). ? Institutional inquiries regarding enterprise licensing should be directed to David Grant, Senior Vice President ? Sales, at dag@insmark.com or (925) 543-0513.

Testimonials

"InsMark is the Picasso of the financial services world ? their marketing savvy never fails to amaze me."

Doug Peete, Past President, Top of the Table, InsMark Silver Power Producer, Overland Park, KS

“The InsMark Illustration System has significantly enhanced my life insurance production scope. I feel I can now present my ideas with superb backup support material.”

Ross Hoffman, Ventura, CA