Several readers contacted me about Blog #37: How to Smite a Termite asking what it would look like if I compared Dr. Rand’s Indexed Universal Life (IUL) to term insurance coupled with an equity account. So here it is . . .

If an equity account is used for the side fund, the results aren’t all that much different than those in Blog #37, and IUL remains the superior solution.

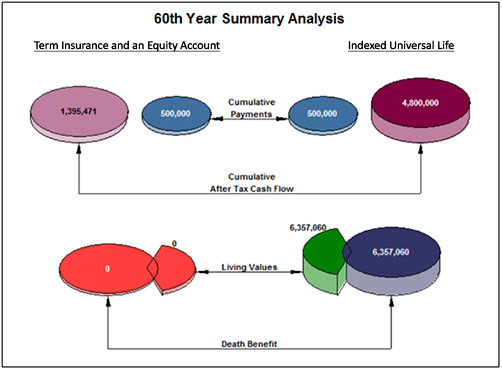

Case Study #1

Equity Account Assumptions

Illustration Years: Age 40 to 100

Growth of Equity Account: 7.50%

Sales Charge: 0%

Mgt. Fee: 0.75% (unusually low -- most advisers charge 1.00% to 1.50%)

Income Tax Bracket: 45% (including a conservative amount for state income tax)

Capital Gains Tax Bracket: 25% (including a conservative amount for state capital gains tax)

Portion of Realized Gains That Is Long-Term: 70% (generous)

Portion of Realized Gains That Is Short-Term: 30% (equally generous)

Portfolio Turnover: 10% (unusually low -- assumes an index-type fund)

30-Year Level Term Insurance: $3,000 a year premium for $3,600,000

(which expires by Dr. Rand’s age 70)

Below is a graphical summary of the results:

Click here to view the IUL vs. Term Insurance and an Equity Account illustration using the above assumptions for the equity account. In this case, the term insurance expires at age 70, and the equity account runs out of gas in year 32 at Dr. Rand’s age 72. The term and equity combination are distinctly in second place. Please be sure to review Pages 8 - 13 due to the backup detail required for the various equity account charges.

Case Study #2

Reducing the Term Insurance to $1,800,000

The term alternative does have an advantage in Case Study #1. In years 1 - 30, the overall death benefit of the combination package is greater than the death benefit of the IUL. ?Since one of the primary purposes of the transaction is to maximize long-range, after tax, retirement cash flow, I believe this is a tolerable difference. But perhaps a fairer comparison would be to reduce the amount of term insurance, say, in half to $1,800,000. Now the death benefit of the term and equity package is only slightly ahead in two years (years 29 and 30), and the term runs out at the end of year 30. Using the same assumptions for the equity account as Case Study #1, the equity account collapses in year 33 at Dr. Rand’s age 73 -- again leaving the term and equity combination still distinctly in second place.

Click here to view this alternate variation. Again, please be sure to review Pages 8 - 13 due to the backup detail required for the various equity account charges.

A Word of Caution: Responsible producers should remain in a long-range advisory position with owners of cash value policies where substantial policy loans are expected since, if a surrender or inadvertent lapse of the IUL occurs in later years, the tax consequence could be onerous. This is one reason I illustrated substantial long-range residual cash value in Dr. Rand’s IUL illustrations. Some life insurance companies have developed concierge units to help monitor such plans.

We’ve been promising for weeks to show you how Dr. Rand intends to use her IUL policy in a Deferred Compensation scenario. We will do that for sure next week in Blog #40 (February 13, 2014).

We used the InsMark Illustration System to prepare the illustrations for this Blog. With that System, you can also compare IUL with taxable, tax exempt, and tax deferred accounts. (They lose, too -- significantly so when participating loans on the IUL are illustrated.)

If you are licensed (or become licensed) for the InsMark Illustration System and would like to review the menu prompts we used for this analysis, please email us at bob@robert-b-ritter-jr.com, and we will get the Case Data file (Workbook) right out to you. Be sure to ask for the Workbook for Blog #39: More on the Magic of Indexed Universal Life.

Click here to learn more about the InsMark Illustration System. You can also contact Julie Nayeri at julien@insmark.com or 888-InsMark (467-6275). Institutional inquiries should be directed to David Grant, Senior Vice President ? Sales, at dag@insmark.com or 925-543-0513.

Testimonials:

“The reason I use InsMark products is because they are so good at explaining financial concepts to all three parties: 1) the producer trying to explain the idea; 2) the computer technician trying to illustrate it; 3) the customer trying to understand it.”

Rich Lindsay, CLU, AEP, ChFC,

Pasadena, CA

The InsMark Illustration System is one of the best sales tools I’ve ever seen for financial professionals to show their clients the benefits of cash value life insurance when considering solutions for their retirement. What I like most is the ability to do side-by-side comparisons between any number of investment alternatives including a 401K, annuity, CDs, IRA, non-qualified brokerage accounts, etc.

Rick Biggert, CLU, President, Retirement Solutions,

Tulsa, OK