(Click here for Blog Archive)

(Click here for Blog Index)

(Presentations in this Blog were created using InsMark’s Wealthy and Wise® System.)

|

|

Blog #196 completes a series of four Blogs featuring InsMark’s CheckMate® Logic as it relates to the purchase of a life insurance policy. Blog #193 (Part 1) dealt with procrastinating clients who seem to want the coverage but postpone purchasing it. Blog #194 (Part 2) dealt with clients who are concerned that cash value life insurance may be inappropriate for retirement planning. Blog #195 (Part 3) deals with clients who want to look at “buy term and invest the difference”. Blog #196 (Part 4) deals with clients who want a comprehensive analysis to see the specific impact on their retirement plan of 1) acquiring the policy compared to 2) investing in an equity account compared to 3) buying term insurance and investing the difference. I will cover all four points in detail from the Main Platform at the 2020 InsMark Symposium in Las Vegas on February 28 – 29. I look forward to seeing you there. |

Case Study

You met Harvey Pierce, MD, in Blog #193, Blog #194 and Blog #195. He and his wife, Grace, are both age 45 and are in a combined, federal and state, income tax bracket of 40%. He has been considering the following cash value life insurance policy:

Indexed Universal Life (IUL) illustrated at 6.85% as follows: $650,000 of increasing death benefit with 20 annual premiums of $30,000 and $120,000 of yearly participating policy loans from age 65 to 100.

Harvey also considered term insurance as a substitute for the IUL. (Blog #195 dealt with this issue, proving IUL to be preferable to “buy term and invest the difference” by a considerable margin.)

Harvey and Grace want to determine how either term insurance or IUL will integrate into their current retirement plan. InsMark’s Wealthy and Wise® is a useful tool to evaluate either option.

It may seem to some of my readers that the comparative analysis in Blog #195 is sufficient to prove the advantages of IUL vs. term insurance so why take this extra step of integrating the comparison within a client’s retirement plan. There are two reasons:

- Many of you already feature retirement planning using an overall analysis of wealth and wealth management. For such professionals, integrating insurance alternatives is a natural extension of your current plan designs if you believe that life insurance – particularly IUL – plays a crucial role in overall retirement planning.

- Those of you who haven’t experienced this form of wealth and retirement planning need to embrace it due to its effectiveness. The results that follow will prove this point.

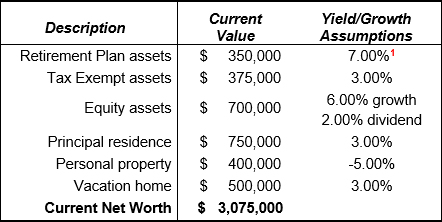

Below is a summary of Harvey and Grace’s current net worth.

| Current Net Worth |

| Harvey and Grace Pierce |

| 1 | Continuing contributions of $19,000 increasing by 2.00% a year with a 25% match by Harvey’s employer. |

Click here for comments regarding yields, sequence of returns, and Monte Carlo simulations.

Retirement Cash Flow Goal

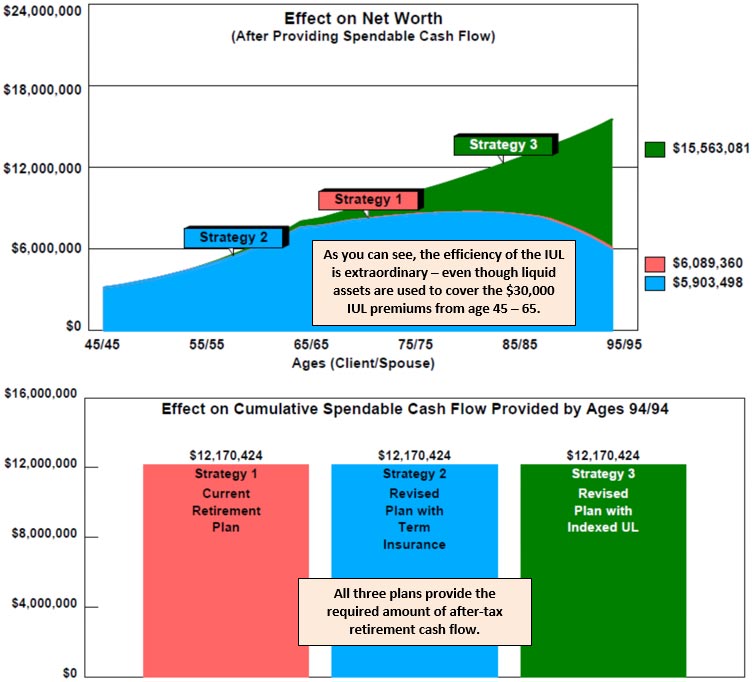

Harvey and Grace would like to have $25,000 a month in after-tax retirement cash flow with a 2.00% cost of living assumption starting at age 65. Extending the analysis to their age 95 requires $9,000,000 of cumulative cash flow ($25,000 x 12 months x 30 years). The 2.00% indexing increases the total cash flow requirement to $12,170,424 between ages 65 and 95 – five years past their joint life expectancy. (Joint life expectancy indicates that at least one spouse is presumed alive.)

Below is a graphic view of the comparison between their current retirement plan vs. an altered version enabled by integrating $650,000 of 20-year level term (premium: $700).

| Image 1 |

| Strategy 1: Current Retirement Plan |

| Strategy 2: Revised Retirement Plan |

| (including $650,000 of term insurance) |

Source: Wealthy and Wise

Let’s see how the IUL performs within the overall retirement plan.

| Image 2 |

| Strategy 1: Current Retirement Plan |

| Strategy 2: Revised Retirement Plan |

| (including $650,000 of term insurance) |

| Strategy 3: Revised Retirement Plan |

| (including $650,000 of Indexed Universal Life) |

Source: Wealthy and Wise

Click here to review all the Wealthy and Wise output associated with this Blog. This analysis contains 51 data ledgers and several graphics totaling 102 pages. That number of ledgers is not as tedious to review as you might think as most of them extend to two pages due to the number of years in the evaluation. Also, Sections 2 through 4 contain many of the same ledgers which are deliberately included to provide you with easy reference to backup information.

With a Wealthy and Wise evaluation, I recommend you have all ledgers for a given case with you when visiting with a client or client’s attorney or CPA. Wealthy and Wise backs up every number shown, and you never know which report you’ll need to answer the inevitable question, “Where did this number come from?”

Many Wealthy and Wise users select a few critical reports in a central section and put the balance in an Appendix. You can create a more elaborate report organization (e.g., Table of Contents and Section pages) by selecting the following prompt available at the bottom right of the Main Workbook Window of Wealthy and Wise:

Conclusion

With the considerable increase in long-range net worth, the Pierces may want to plan for additional cash flow during retirement years for such items as personal use if inflation exceeds the plan’s assumptions, travel, helping grandchildren with college costs, funding of expenses for long-term care, and – possibly – a Roth conversion after age 59 1/2.

So the next time a critic asks Harvey and Grace something like this, “Why would you want to spend $30,000 for something you could get for $700,” they can turn it around and say, “The reason we are spending $30,000 instead of $700 is for a potential increase of $9.6 million in our long-range net worth.”

And don't overlook this critical advantage of the Wealthy and Wise analysis: When the term and the IUL are both presented as individual decisions (as shown in Blogs #194 and #195), the term cost of $700 a year for twenty years or the IUL cost of $30,000 a year for twenty years is an out-of-pocket cost. Wealthy and Wise produces the funds for either choice from its liquid assets, so there is no out-of-pocket client cost for either life insurance option. This result is one of the primary reasons for utilizing a Wealthy and Wise analysis for upper-end clients (where sufficient liquid assets are usually present).

Whole Life Alternative

Although this Blog features IUL, those who prefer the guarantees of Whole Life can produce proportionate results using Wealthy and Wise for more conservative clients. You can do this by reducing the internal asset and income assumptions to align more closely with each client’s risk tolerance.

Suitability

“Suitability” is core to the recommendation of any financial product. FINRA, for example, is quite specific regarding reasonable-basis suitability, customer-specific suitability, and quantitative suitability. One of the best FINRA-approved compliance questionnaires I have seen is from Backroom Technician by Advisys, Inc., which has granted InsMark permission to provide my readers with a copy.

Click here to contact Backroom Technician for more information on its overall product line.

Suze Orman, Dave Ramsey, and Jim Dahle, MD (White Coat Investor®)

American humorist Josh Billings once said that “It ain’t ignorance causes so much trouble; it’s folks knowing so much that ain’t so.”

Don’t let your clients get trapped believing the “buy term and invest the difference” misrepresentations from Suze Orman, Dave Ramsey, and Jim Dahle, MD (White Coat Investor). Their advice is words and uninformed opinion only. Provided your clients have the available cash flow to consider permanent life insurance, let year-by-year comparative mathematics guide their decisions (something Suze, Dave, and Jim don’t include in their exaggerated narratives about permanent life insurance).

Licensing InsMark Systems

To license the Wealthy and Wise, contact Julie Nayeri at julien@insmark.com or 888-InsMark (467-6275) or visit us online. Institutional inquiries should be directed to David Grant, Senior Vice President – Sales, at dag@insmark.com or (925) 543-0513.

InsMark’s Digital Workbook Files

If you would like some help creating customized versions of the presentations in this Blog for your clients, watch the video below on how to download and use InsMark’s Digital Workbook Files.

Digital Workbook Files For This Blog

New Zip File Downloaders

Watch the video.

Experienced Zip File Downloaders Download the zip file, open it, and double click the Workbook file name to open it in your InsMark System.

|

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark System. Please forward it to your PC where your InsMark System(s) are installed. |

If you obtain the digital workbook for Blog #196, click here for a user guide to its content.

For help on how to use InsMark software, go to The Quickest Way To Learn InsMark.

Testimonials

“InsMark has created without question the best suite of software for our industry that has ever existed. I personally have been using their software for almost 30 years, and it changed my career. This unique and user friendly software will add many thousands to your income for as long as you’re in business. InsMark makes me look good, and it will you as well.”

Simon Singer, CFP®, CAP®, RFC®, Past President International Forum, InsMark Platinum Power Producer®, Encino, CA

“I really thought I knew all the sales techniques that affect my business, but I do now, thanks to InsMark.”

Sam Keck, MBA, CLU, CFP, LUTCF, InsMark Platinum Power Producer®, Financial Planner, Denver, CO

“InsMark is the Picasso of the financial services world — their marketing savvy never fails to amaze me.”

Doug Peete, Past President, Top of the Table, and InsMark Power Producer, Overland Park, KS

“The reason I use InsMark products is because they are so good at explaining financial concepts to all three parties: 1) the producer trying to explain the idea; 2) the computer technician trying to illustrate it; 3) the customer trying to understand it.”

Rich Linsday, CLU, AEP, ChFC, InsMark Platinum Power Producer®, Top of the Table, International Forum, Pasadena, CA

“InsMark has increased my production by 10 fold. It clearly communicates to the client the best financial scenario to take.”

Gary Sipos, M.B.A., A.I.F.® InsMark Platinum Power Producer®, Sipos Insurance Services, Freehold, NJ

“White Coat Investor” is a registered trademark of The White Coat Investor, LLC.

“InsMark”, “Wealthy and Wise” and “CheckMate” are registered trademarks of InsMark, Inc.

Copyright © 2019 InsMark, Inc.

All Rights Reserved

Important Note #1: The hypothetical values associated with this Blog assume the nonguaranteed values shown continue in all years. This is not likely, and actual results may be more or less favorable. Life insurance illustrations are not valid unless accompanied by a basic illustration from the issuing life insurance company.

Important Note #2: The information in this Blog is for educational purposes only. In all cases, the approval of a client’s legal and tax advisers must be secured regarding the implementation or modification of any planning technique as well as the applicability and consequences of new cases, rulings, or legislation upon existing or impending plans.

Important Note #3: Many of you are rightly concerned about the potential tax bomb in life insurance that can accidentally be triggered by a careless policyowner when policy loans are present and net cash values are so low that the income tax on the gain on surrender (calculated using gross cash values less basis) is more – often significantly more – than the net cash surrender value.

This lurking tax bomb can be present in all forms of whole life and universal life where policy loans of any type are utilized. It can be avoided, and you, the producer, are key to making sure your clients are aware of how to sidestep it.

A tax bomb can be avoided if the policy is neither surrendered nor allowed to lapse, since the policy death benefit wipes away the income tax liability. The foundation of this special treatment is IRC Section 101. This statute provides that the proceeds of life insurance maturing as a death claim are exempt from federal income tax. This applies to the full death benefit, including any cash value component whether loans exist or not.

Can your clients remember these facts years into the future? If they are incapacitated, will family members understand the issues? It is probably best to file a short note with the policy – something like this (although your compliance officer will likely have preferred language):

If/when you take policy loans on this policy, be sure to talk to your financial adviser before surrendering or lapsing the policy in order to anticipate unexpected tax consequences that may otherwise be avoided.

Some life insurance companies have concierge units that monitor loan status at the point of lapse or surrender, and you would be well-advised to select an insurance company with this capacity. To be effective regarding the tax bomb, such carriers need to be proactive in their client relationships, not merely reactive to client inquiries. I hope that ultimately the policyholder service division of all life insurance companies will bring this potential liability to the attention of those surrendering or lapsing policies, particularly those policies with 50% or more of the gross cash value subject to outstanding loans.