(Click here for Blog Archive)

(Click here for Blog Index)

(Presentations in this Blog were created using InsMark’s Wealthy and Wise® System.)

|

This Blog addresses an awkward situation. James and Allison McNamara are both age 55 with a current net worth of $4.75 million. They are at the peak of their earning (and saving) years and intend to retire at age 65. They are reviewing an Indexed Universal Life (IUL) presentation involving a Private Retirement Plan (PRP).

Some people think IUL does not work very well with loan activity starting as early as ten years. This presents a dilemma that involves the difficult task of demonstrating to James and Allison the value of a retirement strategy that produces no retirement cash flow for 20 years – 10 years after retirement begins.

To address this, you cannot rely on the usual illustration format and try to talk your way through the problem as the issue is so obvious; however, our Wealthy and Wise® System can handle it easily since the System merely finds the needed retirement cash flow from other assets. The results of this analysis should open up a whole new market segment for Private Retirement Plan presentations, i.e., those at or near retirement with large sums available for retirement savings but who would usually pass on a plan that doesn’t begin to produce income until well past retirement.

| Below is a summary of James and Allison’s current net worth: | |

|---|---|

| $ 2,000,000 | Equity Assets @ 6.50% growth; 1.00% dividend |

| 500,000 | Taxable Assets @ 5.00% |

| 600,000 | Tax Exempt Assets @ 4.00% |

| 500,000 | Retirement Plan Assets @ 7.50% |

| 850,000 | Principal Residence1 @ 3.00% growth |

| 400,000 | Personal Property @ -5.00% growth |

| 300,000 | Rare Coin Collection @ 6.00% growth |

| 500,000 | Vacation Home @ 3.00% growth |

| $ 5,500,000 | Total Net Worth |

| 1They intend to sell their principal residence at retirement and move to their vacation home. |

Click here for comments on yields and Monte Carlo simulations.

Case Study

James and Allison are in a 37% tax bracket which they expect will reduce to 30% at retirement. They would like to have at least $250,000 a year in after tax cash flow at retirement, and they want to include 3.00% indexing as an inflation offset. Between their retirement and age 100, this will require $15,115,521 of after tax cash flow. They do not want their net worth to diminish after they retire.

Strategy 1 will reflect the McNamaras’ current situation.

Strategy 2 will be identical to Strategy 1 with the exception that it will include $1,863,066 million of IUL insuring Allison. (James has a couple of medical issues that indicates Allison is the preferred insured.) The IUL has scheduled premiums of $100,000 a year for six years with policy loans of $150,000 beginning in year 21 (age 75), ten years after they retire. These loans will supply a substantial portion of their needed retirement cash flow, leaving other assets to accumulate more rapidly.

Click here to review the IUL report. The illustration includes participating policy loans (cash values securing these loans continue to participate in whatever indexed interest is credited to the policy). This feature can produce significantly better results than fixed loans which is why I tend to illustrate IUL in situations involving policy loans for retirement cash flow. For a demonstration of this, see my Blog #52: Participating Loans vs. Fixed Loans. (Whole life cannot compete with this feature.)

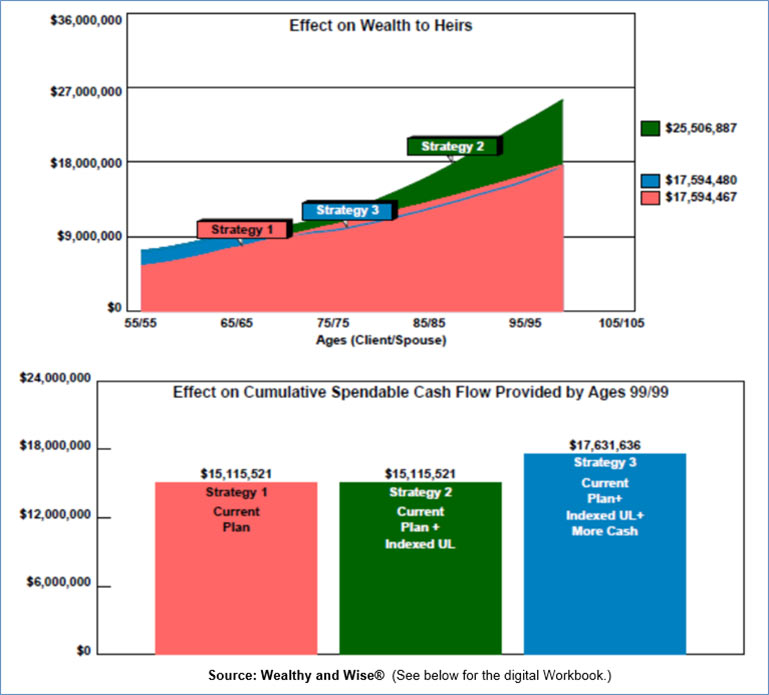

The key to the power of this analysis lies in your understanding that Strategy 2 does not require James and Allison to “spend” $100,000 of their current income for the next six years to fund the policy. Instead, Wealthy and Wise finds the cash flow for the premium from their existing assets, i.e., asset reallocation. The results may surprise you because not only does their asset base provide the premiums for the life insurance, it will cost James and Allison almost $8 million in illustrated long-range net worth and wealth to heirs if they don’t acquire this policy! You can see this effect in the graphic below.

| Image 1 |

| Current Plan |

| vs. |

| Current Plan + Indexed Universal Life |

Their long-range net worth is increased by almost 145%, and as you can see below, wealth to heirs is similarly enhanced.

| Image 2 |

| Current Plan |

| vs. |

| Current Plan + Indexed Universal Life |

Imagine this conversation:

James: “That looks great, but instead of growing net worth to over $25 million, what if we withdrew more cash flow.”

Allison: “We’d like to have a cash flow cushion for travel and supplemental medical costs as well as help the grandchildren with some of their needs, like education or down payments on a house.”

The precise answer for James and Allison is $71,889 of additional after tax cash flow is available to them every year from age 65, when they retire, through age 100. (I was able to tell the McNamaras this number accurately in about 30 seconds. Access to a report on how you can calculate this using the new Cash Flow Availability Calculator in our Wealthy and Wise software is available below.)

James: “What I like about this approach is that we would still have plenty of cushion in case of any financial ups and downs.”

Below is the revised net worth and cash flow graphic. Strategy 3 produces $2,516,115 ($71,889 x 35 years) more supplemental cash flow with net worth ending up virtually identical to Strategy 1 – all caused by the presence of the IUL.

| Image 3 |

| Current Plan |

| vs. |

| Current Plan + Indexed Universal Life |

| vs. |

| Current Plan + Indexed Universal Life + Additional Cash Flow |

Below are the revised graphics for wealth to heirs and cumulative cash flow for the McNamaras including the Strategy 3 assumptions.

| Image 4 |

| Current Plan |

| vs. |

| Current Plan + Indexed Universal Life |

| vs. |

| Current Plan + Indexed Universal Life + Additional Cash Flow |

Wealthy and Wise Reports

Click here to review the 38 Wealthy and Wise reports associated with Strategies 1, 2, and 3. That is a lot to consider, I know; however, I recommend that you have all the reports for a specific client in your possession particularly if you are visiting with a client’s attorney or CPA. Wealthy and Wise backs up every number shown, and you will likely need access to some of the reports for the multiple times you get asked this question by a client, attorney, or CPA: “How was this number calculated?” Incidentally, those professional advisers are typically very impressed with the scope of Wealthy and Wise.

Many Wealthy and Wise users select a few critical illustrations in the main section and put the balance in an Appendix. You can accomplish more elaborate report organization by adding a Table of Contents and Section pages which I did by selecting the following prompt available at the bottom right of the Workbook Main Window:

Conclusion

As you can see, the strategy of including investment-grade life insurance in a retirement plan is effective – particularly IUL with participating loans. Virtually every age group can generate remarkable results with this technique – even those close to, or in, retirement. There is a similar analysis in Blog #150 for a couple both age 60 and another in Blog #58 for a couple in their 40s. I have seen its effectiveness even at age 70.

Cash Flow Availability Calculator

$71,889 a year for 35 years (age 65 to 100) in addition to the indexed retirement cash flow of $250,000 for 35 years is very significant. How is this calculated?

Click here for the essential details of the Cash Flow Availability Calculator in Wealthy and Wise that was used for Strategy 3.

Final Thought #1

I know that many of my readers are comfortable selling the retirement cash flow features of IUL using a stand-alone illustration not integrated with a client’s other assets. Clients typically consider the premiums for such plans to be an expense. Changing to a Wealthy and Wise analysis creates a new learning curve because your presentation changes to an asset transfer. Believe this: the wealthier a client, the easier it is to convince him or her of the power of integrating IUL into their portfolio of assets with this type of analysis. With allocations from current assets as the source of the IUL premiums as shown in this Blog, it becomes a case of “comparing assets and cash flow if you do it – with what happens if you don’t”. That is an entirely different presentation that can have compelling results for you. With some clients, Strategy 2 (greater net worth) will be sufficient; others will be very impressed (perhaps even astonished) with your Strategy 3 logic (greater cash flow) – or, maybe, somewhere in between.

The payoff? You will develop much higher average compensation per case, and a client locked into your planning expertise, not just an IUL policyholder. Tended to carefully, you will likely have this client for life.

If you are an experienced user with Wealthy and Wise, putting a case together like this will be relatively straightforward. (See below to obtain the electronic Workbook I used to prepare the data for all the Strategies evaluated in this Blog.)

That’s the good news. The bad news for some is that you have to gather all of your client’s financial data for this type of analysis. How do you feel about asking a prospective client to reveal details of economic data? You have to earn a potential client’s confidence to do that. My suggestion for the best way to gain that confidence is to share examples of how this concept works for others – this Blog, for example, or the Wealthy and Wise reports associated with it.

Note: A Fact Finder is available in Wealthy and Wise to guide you in your data gathering (see Tools on the main menu bar). Many of our licensees tell me they think the Fact Finder is best filled out with the client(s) present and involved in the process.

At first glance, the Fact Finder may look intimidating, but on most pages, you will be entering data in only a few of the listed categories. To acquaint yourself with it, try filling one out for your situation. Then enter that data in your Wealthy and Wise System – you may be pleasantly surprised.

Final Thought #2

I am frequently asked if a Wealthy and Wise analysis can be reliable projected so far into the future. A plan like this cannot be reliably projected if you perceive retirement planning as a “one and done” analysis. To be a dependable adviser to your clients, you must meet with them at least once a year and bring all the data current. Each year represents a fresh look at the future, and this is what turns prospects into clients, not just policyholders. If you follow this procedure, soon your clients won’t make a significant financial move without asking you to run it through Wealthy and Wise. Otherwise, changes in finances will make your original evaluation obsolete, and you will lose clients to other advisers.

This approach also gives you a sound basis for charging an annual monitoring fee for the analysis. If you can develop fee revenue from clients who are glued to you for service, it has a significant impact on the value of your practice. These days, recurring revenue is hard to develop, and monitoring fees are an excellent way to do so. Blog #98: The Value of “You” to Your Clients (Part 2 of 2) covers this issue in detail including how to include such fees within a presentation so they are paid for out of plan assets not by addition out-of-pocket costs by the client. Be sure to check with compliance if you are considering monitoring fees.

If you prefer a “one and done” solution, comprehensive retirement planning is not for you. That is not to say there isn’t plenty of opportunity for you – just not in this field.

Licensing InsMark Systems

To license Wealthy and Wise, visit us online or contact Julie Nayeri at Julien@insmark.com or 888-InsMark (467-6275). Institutional inquiries should be directed to David Grant, Senior Vice President — Sales, at dag@insmark.com or (925) 543-0513.

Creating Similar Presentations

If you would like some help creating customized versions of the presentations in this Blog for your clients, watch the video below on how to download and use InsMark’s Digital Workbook Files.

Digital Workbook Files For This Blog

New Zip File Downloaders

Watch the video.

Experienced Zip File Downloaders Download the zip file, open it, and double click the Workbook file name to open it in your InsMark System.

|

Before downloading and reviewing any files, be certain you have installed the most current updates to your Wealthy and Wise and InsMark Illustration System. Do this using Live Update available under Help on the main menu bar of the System or this icon on the main menu bar:

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark Systems. Please forward the Workbook where you can launch it on your PC where your InsMark System(s) are installed. |

If you obtain the digital workbook for Blog #183, Click here for a guide to its content. It will be invaluable to you.

Testimonials

“If you don’t get the client to distinguish cash flow from net worth, you won’t make the case sale. In my experience, Wealthy and Wise is the only system that recognizes this important estate planning component.”

Stephen Rothschild, CLU, ChFC, CRC, RFC, International Forum Member, Saint Louis, MO

“Major cases we are developing have all moved along successfully because of the sublime simplicity and communication capability of Wealthy and Wise. I guarantee that the proper use of this tool will dramatically raise the professional and personal self-image of any associate who dares to take the time to understand it . . .”

Simon Singer, International Forum Member, InsMark Platinum Power Producer®, Encino, CA

“I am writing to give you a ringing endorsement for the Wealthy and Wise System. As you know, I am a LEAP practitioner, and the Wealthy and Wise software has helped me supplement my LEAP skills and increase my commissions. I have been paid for many cases using Wealthy and Wise as support, the smallest of which was $27,000, the largest was $363,000. With those type of commissions, you would have to be nuts not to buy it.”

Vincent M. D’Addona, CLU, ChFC, MSFS, AEP, InsMark Power Producer®, New York, NY

“InsMark helps us help our clients understand their money and their choices. I always learn something new that changes what we do and how we can do it more efficiently. That translates to a better bottom line for us and for our clients. It’s making more money for everyone – just by pushing InsMark buttons on the computer.”

Kay Corbin, CLU, ChFC, InsMark Platinum Power Producer®, Phoenix, AZ

“The InsMark software is indispensable to my entire planning process because it enables me to show my clients that inaction has a price tag. I can’t afford to go without it!”

David McKnight, Author of The Power of Zero, InsMark Gold Power Producer®, Grafton, WI

“InsMark” and “Wealthy and Wise” are registered trademarks of InsMark, Inc.

Important Note #1: The hypothetical values associated with this Blog assume the nonguaranteed values shown continue in all years. This is not likely, and actual results may be more or less favorable. Life insurance illustrations are not valid unless accompanied by a basic illustration from the issuing life insurance company.

Important Note #2: The information in this Blog is for educational purposes only. In all cases, the approval of a client’s legal and tax advisers must be secured regarding the implementation or modification of any planning technique as well as the applicability and consequences of new cases, rulings, or legislation upon existing or impending plans.

Important Note #3: Many of you are rightly concerned about the potential tax bomb in life insurance that can accidentally be triggered by a careless policyowner when policy loans are present and net cash values are so low that the income tax on the gain on surrender (calculated using gross cash values less basis) is more – often significantly more – than the net cash surrender value.

This lurking tax bomb can be present in all forms of whole life and universal life where policy loans of any type are utilized. It can be avoided, and you, the producer, are key to making sure your clients are aware of how to sidestep it.

A tax bomb can be avoided if the policy is neither surrendered nor allowed to lapse, since the policy death benefit wipes away the income tax liability. The foundation of this special treatment is IRC Section 101. This statute provides that the proceeds of life insurance maturing as a death claim are exempt from federal income tax. This applies to the full death benefit, including any cash value component whether loans exist or not.

Can your clients remember these facts years into the future? If they are incapacitated, will family members understand the issues? It is probably best to file a short note with the policy – something like this (although your compliance officer will likely have preferred language):

If/when you take policy loans on this policy, be sure to talk to your financial adviser before surrendering or lapsing the policy in order to anticipate unexpected tax consequences that may otherwise be avoided.

Does this note make it harder or easier to deliver the policy? It’s harder if you haven’t discussed it with your client; easier if you have. And that’s the point – you should discuss it.

Some life insurance companies have concierge units that monitor loan status at the point of lapse or surrender, and you would be well-advised to select an insurance company with this capacity. To be effective regarding the tax bomb, such carriers need to be proactive in their client relationships, not merely reactive to client inquiries. I hope that ultimately the policyholder service division of all life insurance companies will bring this potential liability to the attention of those surrendering or lapsing policies, particularly those policies with 50% or more of the gross cash value subject to outstanding loans.