(Click here for Blog Archive)

(Click here for Blog Index)

(Presentations in this Blog were created using InsMark’s Wealthy and Wise® and the InsMark Illustration System.)

|

Harry and Paige Foster, both age 45, are operators of a lobster boat out of Bass Harbor, Maine. Their only child, Jeremy, graduated in June from Amherst College. Among the family joys celebrated is the final relief from college costs as Harry and Paige have struggled to finance Jeremy’s $200,000 of college costs in order to ensure he could graduate with no student debt. They are currently earning a combined after tax income of $110,000 a year fishing for lobsters.

They are now ready to emphasize accelerated funding of their own retirement plan. Both Harry and Paige have been participating in 401(k) plans, although at a reduced level due to the strain of Jeremy’s college costs. With that out of the way, they both intend to begin making maximum 401(k) contributions of $18,000 a year. In their marginal income tax bracket of 30%, their income tax deduction will reduce the cost of the contribution for each of them from $18,000 to $12,600 (18,000 x 70%).

Inflation

(The Government’s Damage to Currency as a Store of Value)

Inflation issues add a complication to retirement planning. Given the Fosters’ current after tax income of $110,000, is $90,000 a reasonable goal for their spendable cash flow at retirement? It is if you take into account at 65 they each will no longer be contributing a deductible $18,000 into their 401(k) plans.

But $90,000 is not reasonable if you take inflation into account over those 20 pre-retirement years. How much inflation?

Since 1929, inflation has averaged 3.11%. Since 2000, inflation has averaged 2.13%. Click here to view the historical levels of inflation rates.

Examine Table 1 below to see the effect of protecting the buying power of the first $90,000 of cash flow at their ages 65/65:

| Table 1 |

What about inflation after retirement – shouldn’t it be factored in as well? Table 2 below shows quinquennial retirement years up through age 90, the Fosters’ joint life expectancy.

| Table 2 |

As you can see, inflation has a serious impact on retirement planning. If you ignore it, your competition will damage your credibility when they review your plan. The following material illustrates a 2.50% inflation factor in all years.

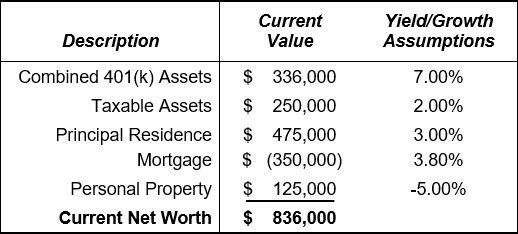

With inflation in mind, let’s start the retirement planning for Harry and Paige. Below is a summary of their current net worth.

| Current Net Worth |

| Harry and Paige Foster |

Click here for comments regarding yields, sequence of returns, and Monte Carlo simulations.

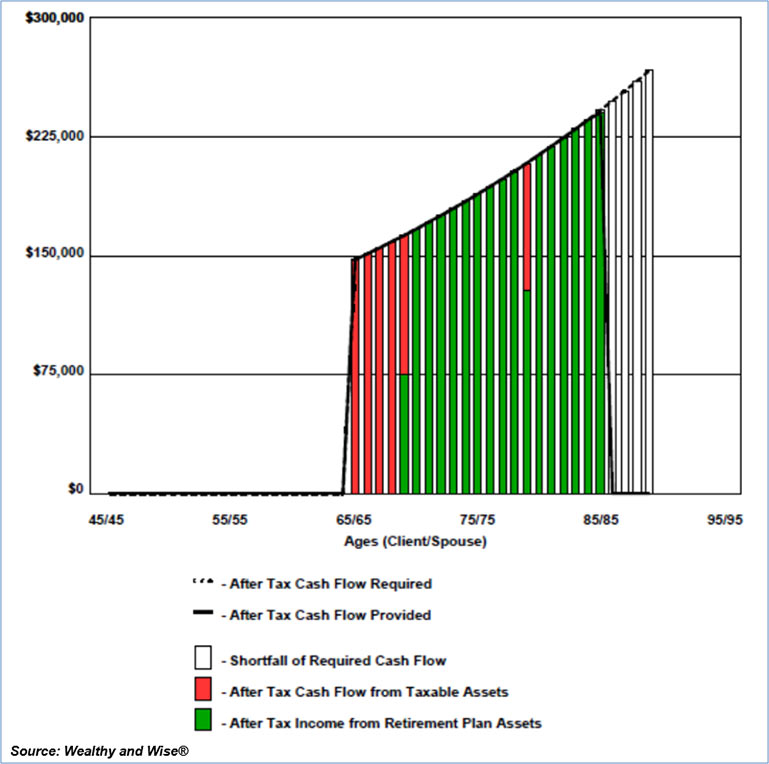

Let’s see how their current retirement plan1 performs in producing $90,000 of 2.50% indexed, spendable, cash flow at retirement.

1The Fosters believe the Social Security Trust Fund is unsustainable, and they don’t expect to collect retirement benefits from this source. This analysis therefore excludes this source of cash flow.

| Image 1 |

| Strategy 1 – Current Plan |

| Sources of Cash Flow |

Cash flow and liquid assets run out at their age 82; only illiquid home equity remains and a small amount of depreciating personal assets.

Let’s look at a revised plan where we downsize their home at retirement. This will release some capital to add to their liquid assets with the goal of extending their years of spendable cash flow. Click here for the Wealthy and Wise® tax calculation on downsizing at age 65 that seems reasonable to the Fosters that produces a little over $400,000 of additional investable funds as they begin their retirement.

Here are the new spendable cash flow results:

| Image 2 |

| Strategy 2 – Downsize Home at Retirement |

| Sources of Cash Flow |

We have moved the dial a little – cash flow and liquid assets run out at the Fosters’ age 85, still five years short of their joint life expectancy at age 90.

Within the framework of their current asset allocation, there doesn’t appear to be any remaining alternative that will meet their desired retirement cash flow. Except one: Let’s examine what happens if we divert the $12,600 after tax cost of each of their $18,000 401(k) contributions to Indexed Universal Life (“IUL”).

| Indexed Universal Life |

| Harry and Paige Foster |

2from the Illustration of Values module in the InsMark Illustration System.

Click here to review the Illustration for Harry Foster, and click here to review the Illustration for Paige Foster.

The two policies are max-funded in order to develop the most cash value possible which, in turn, produces the most in income tax free policy loans.

| Image 3 |

| Strategy 3 – Convert 401(k) Contributions to IUL |

| Sources of Cash Flow |

-Contributions-to-IUL-Sources-of-Cash-Flow-769x746.jpg)

The indexed $90,000 of spendable cash flow is now accomplished as the IUL has completed their plan in Strategy 3.

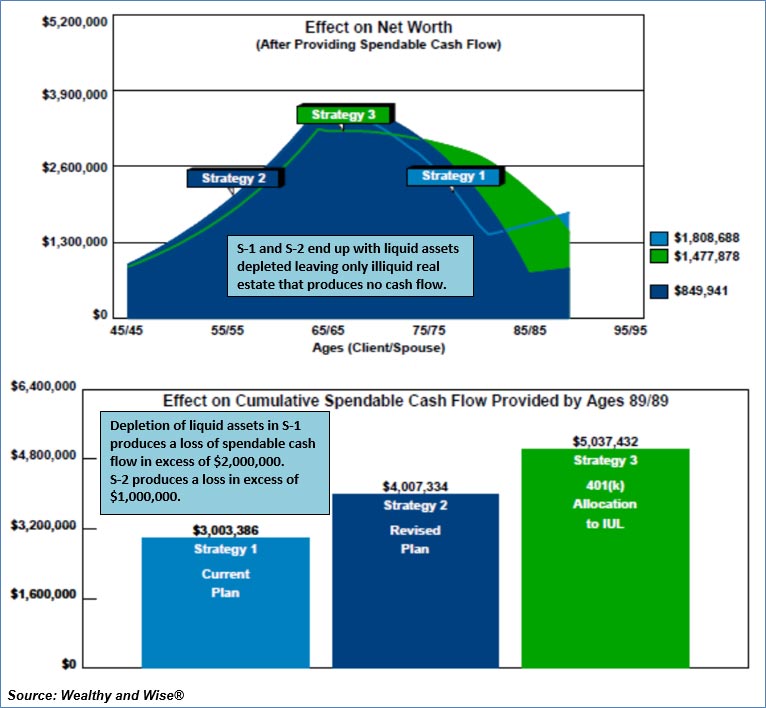

Below is a net worth comparison of each alternative discussed above.

| Image 4 |

| Comparison of Net Worth |

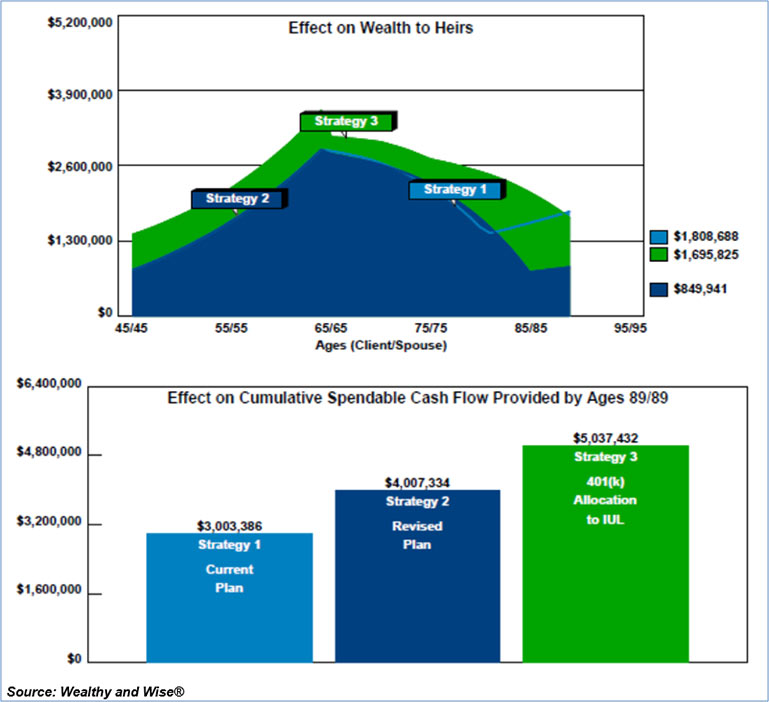

Strategies 1 and 2 also negatively affect the Fosters’ heirs.

| Image 5 |

| Comparison of Wealth to Heirs |

Strategy 3 has been accomplished with no additional out-of-pocket cost for the Fosters producing what is known as a cash flow neutral analysis.

Issues to Consider

- With their joint life expectancy of age 90, one of the spouses is actuarially likely to survive for additional years. As time progresses, the Fosters should consider adding to their retirement assets – probably by way of more IUL funded by any increases in their after tax income. This will develop a cushion of cash flow beyond age 90. On the other hand, any permanent increases in income will likely increase their desired after tax retirement cash flow. These two issues will require careful, ongoing analysis.

- In order to extend cash flow, the Fosters may want to consider reducing – or even eliminating – inflation indexing after, say, age 85, when its impact may be less significant.

- Additional liquidity could be produced by investing their retirement savings more aggressively than 2.00%. Like so many others, the Fosters have been trapped waiting for taxable interest to increase. Perhaps they should be more aggressive in searching out alternative investments.

- A reverse mortgage on their downsized home could make sense at some point during retirement.

This analysis is not just a “one and done” evaluation. It must be carefully managed with frequent reviews (at least annually) to update data and assumptions. The framework of Wealthy and Wise is particularly suited to do this, and if you proactively don’t do it, you will lose clients to other wealth planners. Assuming you have no compliance prohibitions against it, consider charging clients like the Fosters an annual monitoring fee and include its costs in your analysis. (Many of our licensees charge fees for the initial study as well.)

Blog #98: The Value of “You” to Your Clients (Part 2 of 2) involves a Wealthy and Wise case where monitoring fees have been included in the analysis. It involves a premium financing case, but there is serious logic in including monitoring fees in any comprehensive retirement plan.

Wealthy and Wise Reports

Click here to view the 95-page Wealthy and Wise evaluation. That’s not as tedious as you may think as most of the numerical reports run to two pages due to the 45 years in the analysis. That is still a lot of reports, but after all, this is a comprehensive wealth planning evaluation. I don’t know how you can present it professionally without revealing all its components, and I recommend that you have all the reports for a given analysis with you when you are visiting with a client or client’s attorney or CPA. The system backs up every number shown, and you never know which report you’ll need to have handy to answer the inevitable question, “Where did this number come from?”

Most Wealthy and Wise users select a few key illustrations for the main report and put the balance in supplemental sections or an Appendix. More elaborate report organization can be accomplished (Table of Contents and Section pages) through use of the following prompt which I used for this Blog — located on the bottom right of the Main Workbook Window:

InsMark’s Digital Workbook Files

If you would like some help creating customized versions of the presentations in this Blog for your clients, watch the video below on how to download and use InsMark’s Digital Workbook Files.

New Zip File Downloaders

Watch the video.

Experienced Zip File Downloaders Download the zip file, open it, and double click the Workbook file name to open it in your InsMark System.

|

Before downloading any files, be certain you have updated your Wealthy and Wise System to Version 13.0 if you haven’t already done so. Update using Live Update under Help on the main menu bar of either System or this icon on the main menu bar in either System:

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark Systems. Please forward the Workbook where you can launch it on your PC where your InsMark System(s) are installed. |

If you obtain the digital workbook(s) for Blog #165, click here for a guide to its content.

Licensing InsMark Systems

To license any of the InsMark software products, visit our Product Center online or contact Julie Nayeri at Julien@insmark.com or 888-InsMark (467-6275). Institutional inquiries should be directed to David Grant, Senior Vice President — Sales, at dag@insmark.com or (925) 543-0513.

For help on how to use InsMark software, go to The Quickest Way To Learn InsMark.

Testimonials

“If you don’t get the client to distinguish cash flow from net worth, you won’t make the case sale. In my experience, Wealthy and Wise is the only system that recognizes this important estate planning component.”

Stephen Rothschild, CLU, ChFC, CRC, RFC, International Forum Member, Saint Louis, MO

“The InsMark software is indispensable to my entire planning process because it enables me to show my clients that inaction has a price tag. I can’t afford to go without it!”

David McKnight, Author of The Power of Zero, InsMark Gold Power Producer®, Grafton, WI

“I am writing to give you a ringing endorsement for the Wealthy and Wise System. As you know, I am a LEAP practitioner. The Wealthy and Wise software has helped me supplement my LEAP skills in the over age 60 client base. I have been paid for many cases using Wealthy and Wise as support, the smallest of which was $27,000, the largest was $363,000. With those type of commissions, you would have to be nuts not to buy it.”

Vincent M. D’Addona, CLU, ChFC, MSFS, AEP, InsMark Platinum Power Producer®, New York City, NY

“Major cases we are developing have all moved along successfully because of the sublime simplicity and communication capability of Wealthy and Wise. I guarantee that the proper use of this tool will dramatically raise the professional and personal self-image of any associate who dares to take the time to understand it . . .”

Phillip Barnhill, CLU, InsMark Gold Power Producer®, Minneapolis, MN

Important Note #1: The hypothetical values associated with this Blog assume the nonguaranteed values shown continue in all years. This is not likely, and actual results may be more or less favorable. Life insurance illustrations are not valid unless accompanied by a basic illustration from the issuing life insurance company.

Important Note #2: Many of you are rightly concerned about the potential tax bomb in life insurance that can accidentally be triggered by a careless policyowner. Click here to read Blog #51: Avoiding the Tax Bomb in Life Insurance.

Important Note #3: The information in this Blog is for educational purposes only. In all cases, the approval of a client’s legal and tax advisers must be secured regarding the implementation or modification of any planning technique as well as the applicability and consequences of new cases, rulings, or legislation upon existing or impending plans.

“InsMark” and “Wealthy and Wise” are registered trademarks of InsMark, Inc.