(Click here for Blog Archive)

(Click here for Blog Index)

(Presentations in this blog were created using Wealthy and Wise®.)

|

Tom and Amy Sexton are both age 60 intending to retire at age 70. They are currently in a 30% income tax bracket. Their retirement goal is $120,000 of annual, spendable cash flow (including Social Security) starting at age 70 indexed for inflation at 3.00%. The indexing increases their starting cash flow number by their age 70 to $161,270 which rises gradually to $291,271 by their joint life expectancy at age 90.

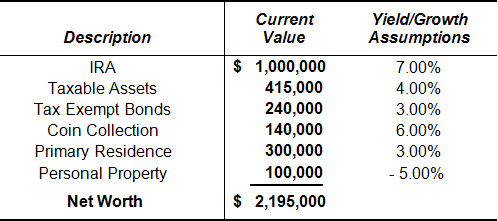

Below is a snapshot of their current net worth:

| Net Worth |

| Tom and Amy Sexton |

Click here for comments regarding yield, growth, and Monte Carlo simulations.

This Blog presents a compelling case for creating retirement income that does not count toward the $32,000 threshold that establishes taxation of Social Security retirement benefits. In Tom and Amy’s case, this includes eliminating: 1) interest on their taxable assets, 2) yields on their tax exempt bonds, and 3) required minimum distributions from the IRA by converting it to a Roth.

|

Loans on life insurance and Roth distributions do not count toward the Social Security $32,000 threshold. Therefore, we rearranged the assets that do apply to the threshold (noted above) to provide cash flow for premiums of $50,000 for five years on $637,000 of indexed universal life (“IUL”) on Tom’s life with participating policy loans starting at age 70. Additional cash flow is directed from these assets to pay the income tax on the Roth conversion in order to provide additional exempt income also starting at their age 70. And, abracadabra, there is no longer any income tax on their Social Security retirement benefits. This results in a serious gain in spendable, retirement cash flow while also maintaining high levels of ongoing net worth. |

|

Taking these steps provided sufficient funds that we were also able to increase their spendable cash flow by 27.7% in each retirement year.

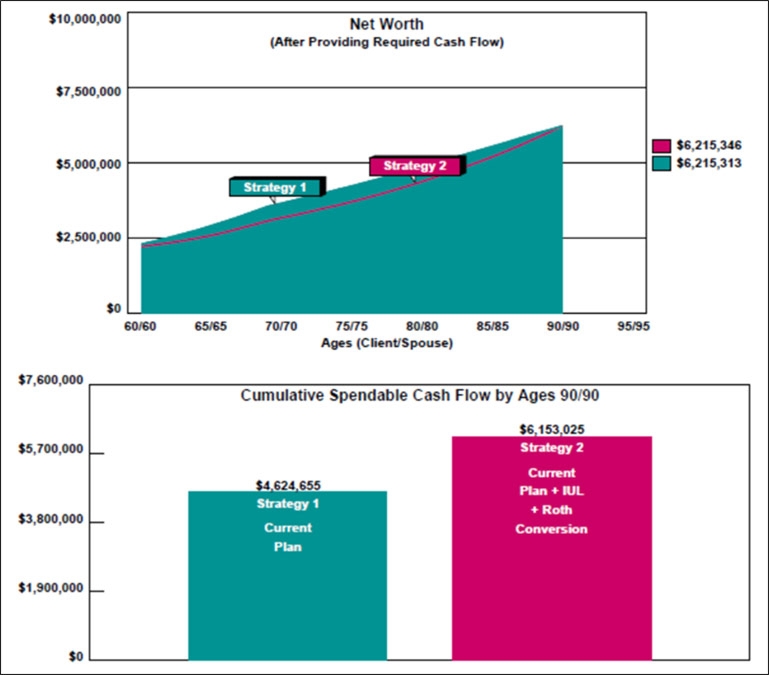

Below is a Wealthy and Wise® comparative graphic of net worth and spendable cash flow.

| Image 1 |

| Net Worth Comparison |

By Tom and Amy’s joint life expectancy of age 90, Strategy 2 has increased their cumulative, spendable, retirement cash flow by $1,530,000.

Click here to review how Wealthy and Wise can easily illustrate the long-range net worth of Strategy 2 being so close to Strategy 1 while also producing the increase in spendable cash flow. This dramatic result can only be accomplished when a Strategy 2 transaction like IUL and/or a Roth conversion increases long-range net worth greater than Strategy 1.

Even though Strategy 1 is well in 2nd place, its net worth is not nearly as effective as shown. A substantial portion of it is deferred income tax on the IRA, the negative effect of which you can see in the following graphic summarizing wealth to heirs.

Below is a similar Wealthy and Wise® comparative graphic of wealth to heirs and spendable cash flow.

| Image 2 |

| Wealth to Heirs Comparison |

|

Click here to review 43 pages of reports from this InsMark Wealthy and Wise evaluation. It is a large number of reports; however, with a Wealthy and Wise presentation, I recommend that you have all the reports for a given analysis with you when you are visiting with a client or client’s attorney or CPA. The system backs up every number shown, and you never know which report you’ll need to have handy to answer the inevitable question, “Where did this number come from?” That’s why I provided all of them to you in this Blog. Most Wealthy and Wise users select a few key illustrations for the main report and put the balance in supplemental sections or an Appendix. More elaborate report organization can be accomplished (Table of Contents and Section pages) through use of the following prompt -- which I used for this Blog -- located on the bottom right of the Main Workbook Window: |

|

Conclusion

Allowing no deduction for payments into Social Security followed by taxation of the benefits when received is a nasty double dip by Washington. Our political hierarchy has a ravenous appetite for taxes; consequently, establishing zero taxes on Social Security retirement benefits is a goal that will be welcomed by most of your clients.

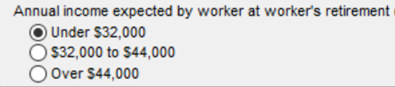

Social Security Calculator

Wealthy and Wise includes a Social Security Calculator for retirement benefits located in any of the dropdowns on the Expected Cash Flow tab. Using a couple as an example, the Calculator allows you to designate taxation of 85% of Social Security benefits if income exceeds $44,000, taxation of 50% of Social Security benefits if income is between $32,000 and $44,000), or no taxation of Social Security benefits if income is under $32,000. This is accomplished through your designation as to which of these three options applies from the following prompt on the Social Security Calculator:

In Tom and Amy Sexton’s situation, when we did the Strategy 1 scenario, we selected “Over $44,000”. Based on the results of Strategy 2 scenario, in order to eliminate taxation of their Social Security benefits, we selected “Under $32,000”.

Note: The InsMark Illustration System also has a Social Security Calculator available on the InsCalc tab that includes retirement, survivor, and disability benefits.

InsMark’s Digital Workbook Files

If you would like some help creating customized versions of the presentations in this Blog for your clients, watch the video below on how to download and use InsMark’s Digital Workbook Files.

Digital Workbook Files For This Blog

Download all workbook files for all blogs

|

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark System. Please forward the Workbook where you can launch it on your PC where your InsMark System(s) are installed. |

Licensing InsMark Systems

To license any of the InsMark software products, visit our Product Center online at or contact Julie Nayeri at Julien@insmark.com or 888-InsMark (467-6275). Institutional inquiries should be directed to David Grant, Senior Vice President - Sales, at dag@insmark.com or (925) 543-0513.

Testimonials

“InsMark has created without question the best suite of software for our industry that has ever existed. I personally have been using their software for almost 30 years, and it changed my career. This unique and user friendly software will add many thousands to your income for as long as you’re in business. InsMark makes me look good, and it will you as well.”

Simon Singer, CFP®, CAP®, RFC®, Past President International Forum, InsMark Platinum Power Producer®, Encino, CA

“I am writing to give you a ringing endorsement for the Wealthy and Wise System. As you know, I am a LEAP practitioner. The Wealthy and Wise software has helped me supplement my LEAP skills in the over age 60 client base. I have been paid for many cases using Wealthy and Wise as support, the smallest of which was $27,000, the largest was $363,000. With those type of commissions, you would have to be nuts not to buy it.”

Vincent M. D’Addona, CLU, ChFC, MSFS, AEP, InsMark Platinum Power Producer®, New York City, NY

“InsMark helps us help our clients understand their money and their choices. I always learn something new that changes what we do and how we can do it more efficiently. That translates to a better bottom line for us and for our clients. It’s making more money for everyone -- just by pushing InsMark buttons on the computer.”

Kay Corbin, CLU, ChFC, InsMark Platinum Power Producer®, Phoenix, AZ

“Major cases we are developing have all moved along successfully because of the sublime simplicity and communication capability of Wealthy and Wise. I guarantee that the proper use of this tool will dramatically raise the professional and personal self-image of any associate who dares to take the time to understand it . . .”

Phillip Barnhill, CLU, InsMark Gold Power Producer®, Minneapolis, MN

If you don’t get the client to distinguish cash flow from net worth, you won’t make the case sale. In my experience, Wealthy and Wise is the only system that recognizes this important estate planning component.”

Stephen Rothschild, CLU, ChFC, CRC, RFC, International Forum Member, Saint Louis, MO

Important Note #1: The hypothetical life insurance illustrations associated with this Blog assumes the nonguaranteed values shown continue in all years. This is not likely, and actual results may be more or less favorable. Actual illustrations are not valid unless accompanied by a basic illustration from the issuing life insurance company.

Important Note #2: Many of you are rightly concerned about the potential tax bomb in life insurance that can accidentally be triggered by a careless policyowner. Click here to read Blog #51: Avoiding the Tax Bomb in Life Insurance.

Important Note #3: The information in this Blog is for educational purposes only. In all cases, the approval of a client’s legal and tax advisers must be secured regarding the implementation or modification of any planning technique as well as the applicability and consequences of new cases, rulings, or legislation upon existing or impending plans.